This article was originally published on Fool.com. All figures quoted in US dollars unless otherwise stated.

Of all the tech titan stocks that have been clobbered this year, Amazon (NASDAQ: AMZN) is arguably one of the more surprising losers. Shares of the e-commerce and cloud computing giant have fallen over 40% so far in 2022. That fall comes despite Amazon holding onto the retail gains it picked up during pandemic lockdowns, and the continual growth in its AWS [Amazon Web Services] cloud segment by a strong double-digit percentage.

Investors weren't pleased with the Q3 2022 report. Management indicated more slowing growth could lie ahead as a record run-up in the dollar (a result of the U.S. Federal Reserve's huge interest rate increases this year). But, despite this weakness, Amazon is putting massive amounts of cash to work to bolster its most important business. Is now a once-in-a-decade buying opportunity for this top tech stock?

Re-allocating investments from e-commerce to tech

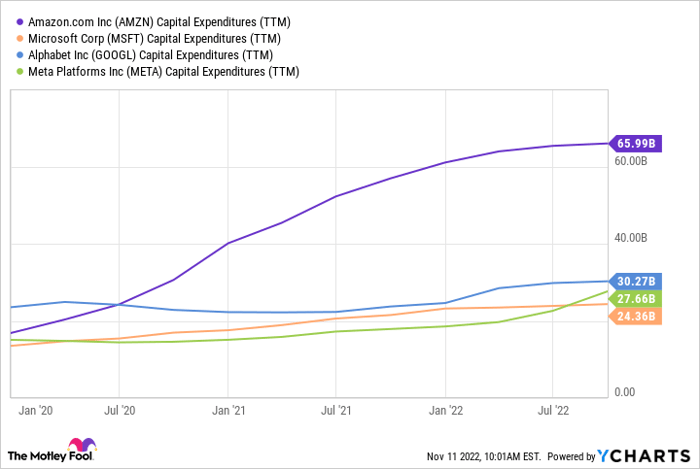

Amazon CFO Brian Olsavsky said on the last earnings call that the company was going to wind up allocating about $60 billion on capital expenditures (or capex, spending on property, plant, and equipment) in 2022. This figure is roughly in line with capex spend in 2021, even though Amazon's growth has slowed significantly. This level of capex also dwarfs the capex spend of fellow tech titans -- even Meta Platforms (NASDAQ: META) and its huge bill on data center equipment in support of its metaverse aspirations.

Data by YCharts

Why does Amazon spend so much more on capex than its peers? For one thing, Amazon isn't just tech. It's also an online retailer. While an online store like Amazon looks like an asset-light business, it isn't. Behind the scenes, Amazon has been spending heavily on things like distribution centers and delivery services to accommodate the explosion of sales it picked up in 2020 and 2021.

But there's something interesting going on with Amazon's capex. Specific numbers were not revealed, but Olsavsky said that $10 billion in capex has been reduced from fulfilment and transportation projects as e-commerce has quieted down. However, that $10 billion has been reallocated to "technology infrastructure, primarily to support the rapid growth, innovation and continued expansion of ... [its] AWS footprint."

Betting big on the business that matters most

This is incredibly significant, especially considering that the AWS cloud computing segment is -- and has been for years now -- the primary engine of Amazon's profitable growth. You see, as great as a seemingly endless collection of products and fast delivery times may be, e-commerce just isn't all that profitable a business for Amazon. Add-on services via Amazon Prime and selling ads within its marketplace are. But at the end of the day, it's AWS that's generating the positive income.

| Amazon segment | First nine months 2022 operating income (Loss) | Operating margin (as % of segment revenue) |

|---|---|---|

| North America | ($2.61 billion) | -1.2% |

| International | ($5.52 billion) | -6.6% |

| AWS | $17.6 billion | 30% |

Data source: Amazon

But why allocate so much extra capex to AWS now, especially given the tough economic climate we're weathering right now? After all, lots of companies out there are cutting spending to boost profits. It was even reported that AWS customers have been working with the company to reduce their spending on the cloud right now, by switching to lower-cost computing workloads and services.

As a result, while AWS has grown revenue by 32% so far in 2022, management indicated Q4 year-over-year growth was trending toward just a mid-20% growth rate. Meanwhile, Amazon has dipped deep into the red as it puts lots of money to work to promote future (and uncertain) growth. Free cash flow (operating income minus capex) was negative $26 billion over the last 12 month stretch.

Nevertheless, Amazon sees a big opportunity, so it's expanding its cloud footprint into new geographies and bolstering its capabilities in existing data centers. Just as disruption from the pandemic forced many organizations around the globe to accelerate their adoption of the cloud, Olsavsky said inflation (especially in energy and computing hardware costs) is having a similar disruptive impact right now. By switching their tech infrastructure to a cloud provider like AWS, a company can ultimately get more flexible with, or reduce, their expenses. Olsavsky explained:

[T]he benefit of cloud computing is really showing up right now because we allow customers to turn what can normally be a fixed expense into a variable expense, and they can let us manage the highs and lows of inflation and other cost of electricity and everything else. And they can get ... to do their business using our services in a very highly secure way. So I think just like in 2020, these time periods are good for long-term adoption on cloud computing. But the offset in the short run is that some companies have demand that drops.

Long story short, Amazon sees behavior-altering changes happening in the economy right now, which spells opportunity for AWS to get aggressive and acquire lots of new customers. Wall Street clearly isn't comfortable with the company spending so heavily, but what else is new? This is far from uncharted territory for Jeff Bezos' empire. If AWS's expansion right now pays off like it has in times past, Amazon stock's giant drop this year can mean opportunity for farsighted investors as well.

Of course, since Amazon has fallen into unprofitability at the moment, it's difficult to accurately stick a fair value on shares. However, management also said it expects to taper down its aggressive spending in the coming years, which would create some earnings leverage. In other words, this stock is incredibly cheap right now. That is, of course, assuming you think Amazon's profitability, as measured by earnings per share, will sharply spike at some point in the next couple of years, and then level back off to a high single-digit or low-teens percentage growth rate after that. (Or if you think free cash flow will spike and turn positive again).

If you have ever felt like you missed the boat on Amazon stock over the last decade, now looks like a prime opportunity to buy.

This article was originally published on Fool.com. All figures quoted in US dollars unless otherwise stated.