If you've ever gone to buy something at the supermarket and noticed it's more expensive than it used to be — that's inflation in action. A little bit of inflation in an economy is a good thing. It means demand is healthy, and people have disposable income. But when inflation gets out of hand, it can have disastrous consequences.

If you're unsure about inflation or why it happens, never fear. This article's for you! Here, we take a deep dive into inflation — by the time you've finished reading, we'll have you speaking like an economist.

What is inflation?

Inflation is when an economy's price of goods and services increases over time. It is measured as the rate of change in a period. For example, if a product that cost $100 last year now costs $103, the annual inflation rate would be 3%.

When inflation occurs, a currency's purchasing power (such as the Australian dollar) decreases. In other words, because prices are rising, people can't afford to buy as much stuff as they used to. They'll need more funds to purchase the same amount of goods or services.

Several factors influence inflation, such as an increase in money supply (usually from government stimulus) or a supply-side shock to raw materials (like a war or natural disaster).

Inflation also doesn't necessarily impact all goods and services in the same way. Certain industries may experience higher price inflation than others, depending on the raw materials they need to produce their products.

In the rest of this article, we'll examine how inflation is measured, what causes it, and its impact on investors.

How is inflation measured?

The inflation figures you'll often hear quoted in the media are typically quite broad. They indicate an economy's overall increase in average prices, which is considered a good indicator of how a country's cost of living changes over time.

However, we can also measure inflation more narrowly – relative to specific goods or services. Inflation rates may differ across products and services, such as groceries, petrol, clothing, or transport. Inflation measures the price change over the relevant period, whatever the underlying product or service.

The Consumer Price Index (CPI) is Australia's most well-known measure of inflation. It measures the percentage change in the price of a basket of household goods and services. The basket represents the goods and services most people regularly use in an economy. So, the CPI is often considered a measure of changes in the cost of living for everyday Australians.

If the price of a particular good or service changes significantly (either up or down), it can impact the overall CPI. For example, if the cost to rent a home increases by 20%, the overall inflation rate can increase because housing is the most widely-used good or service and has the highest weighting in the CPI index.

Similarly, if the price of a commonly used raw material increases, this can also have wide-ranging impacts on the inflation rate. For example, a shock to the global oil supply increases the price of fuel. Higher fuel prices make everything more expensive because the costs of transporting goods or services to the end consumer increase.

Sooner or later, these cost increases get passed on to the consumer, driving up prices and inflation.

But hold on, didn't you say some inflation is healthy?

It's drilled into us from a young age that inflation is terrible. It usually means high interest rates are on the way, with the added spectre of a recession looming on the horizon.

But a little bit of inflation is a good thing — in fact, it's basically unavoidable when the economy is ticking along healthily.

Demand is the lifeblood of the economy. It stimulates the economy — people are out there buying things, and money is moving around freely. It also means more companies are in profit, so they can afford to keep more people employed.

Higher company profits also incentivise more people to start their own businesses, driving product innovation.

The unfortunate by-product of high demand is rising prices. With more people willing to spend money, they eventually begin bidding up the prices of popular goods and services.

Luckily, the economy can tolerate low inflation as long as wage growth can keep up more or less. Generally, we should expect a moderate single-digit inflation rate when the economy is healthy.

This means the economy is growing, but households aren't feeling the pinch of higher prices.

What's the ideal rate?

The Reserve Bank of Australia (RBA) targets an annual inflation rate of 2-3 per cent based on the CPI. When inflation moves outside this bracket, the RBA may use monetary policy (like increasing or decreasing interest rates) to push inflation back within its target range.

Monetary policy impacts the money supply, which in turn impacts prices. When higher interest rates make loans more expensive to repay, fewer businesses borrow money to expand, eventually leading to higher unemployment and lower household income. With less money to spend, demand reduces, prices decrease, and inflation eases.

This rate cycle process can sometimes end in a recession, which is why interest rates are often called a 'blunt tool' in the RBA's fight against inflation.

Who reports inflation figures?

The Australian Bureau of Statistics (ABS) reports the CPI rate every quarter. It declares the quarterly change and calculates an annual rate for the preceding 12 months.

The ABS measures the CPI by collecting the prices of thousands of items. It then calculates the change in price level for each item and aggregates the data to work out the CPI rate.

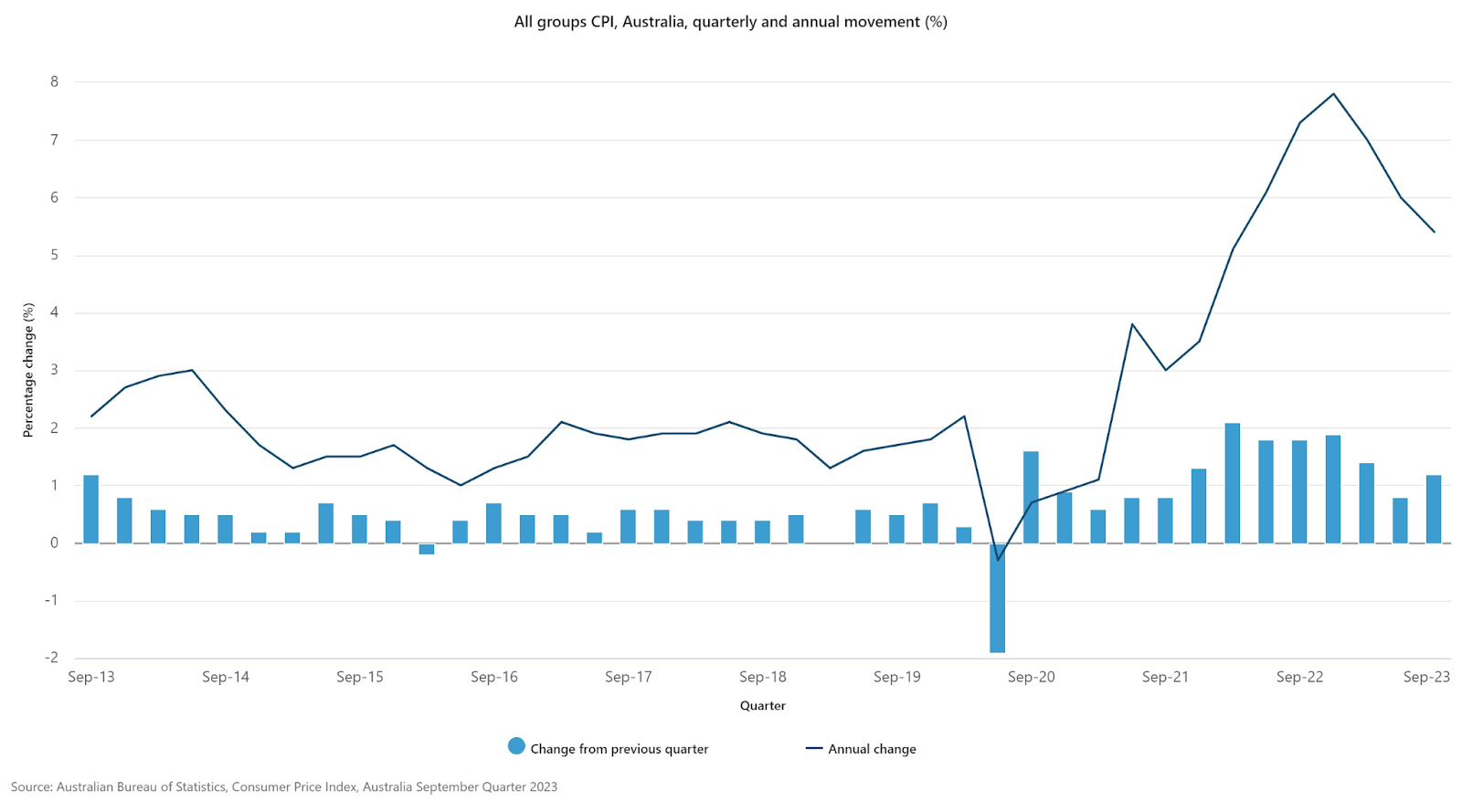

Inflation was 5.4% in Australia over the 12 months to September 2023, with the largest increases coming from insurance and financial services, and housing.

Ironically, rising interest rates could contribute to further inflation by increasing mortgage repayments for landlords, who are subsequently forced to raise the rents on their properties.

The chart below comes courtesy of the ABS and charts the change in inflation over time. While you can see it is now on a clear downtrend after peaking in December 2022, it remains stubbornly high, demonstrating the size of the challenge faced by the RBA.

In the March quarter of 2024, the inflation rate was lower but still sticky at 3.6%.

.

What causes inflation?

There are many potential drivers for inflation. Two of the most common are 'demand-pull' and 'cost-push' inflation. One results from too much demand, while the other is caused by constrained supply.

Demand-pull inflation occurs when an increase of money in the economy lifts the overall demand for products more rapidly than production can keep pace with. Economists often describe this as "too much money chasing after too few goods". People are so flush with cash that they're actually spending too much, bidding up the prices of household goods.

With 'cost-push' inflation, there is an increase in the price of production inputs, like wages or raw materials. These increases work their way down the production line, eventually being passed on to the end consumer and causing the overall prices of goods and services to rise.

We've already discussed the impact that fluctuations in the global oil supply can have on the overall prices of goods and services. But the prices of other raw materials, like energy, iron ore, and copper, can also impact the economy.

Great expectations

Inflation can also be built in and related to expectations. When people see that CPI is increasing, they expect prices to continue rising in the future. This might cause people to make forward purchases (in other words, you may as well buy more stuff now because prices will be higher tomorrow), which increases demand and causes inflation to increase.

Similarly, when inflation is high, workers expect their pay rises to keep up; otherwise, it begins to impact their quality of life. However, rising wages increase household disposable income, further lifting demand for products and services, which causes prices to rise.

The rise in prices increases demand for higher wages, leading to higher production costs. This puts more pressure on prices, creating a spiralling effect.

How does inflation impact shares?

Inflation affects the real returns that ASX investors receive from shares. If you invest $100 today and your investment makes a 5% return, it will be worth $105 in a year. But if the inflation rate is 6%, your money will buy you fewer goods than it could a year ago. This means that its value declined.

Most investors are looking for returns that outpace inflation so they can grow the real value of their investments. The aim is to guard portfolios against the impact of inflation, but it can cause investors to chase ever-higher returns from riskier assets.

Higher inflation rates can put upward pressure on interest rates, as lenders will have to charge their borrowers at least above the inflation rate. A bank doesn't want to reach the end of your loan and receive something back valued less than what they initially loaned you. It's not great business.

Inflation can also result in central banks tightening credit conditions to slow economic growth and lower pricing pressures (which also means higher interest rates).

Higher rates can put downward pressure on the value of some types of investments. This is especially true for more speculative and higher-growth ASX shares that aren't currently profitable, and whose value primarily depends on the market's expectation of their future earnings potential. Think tech shares or emerging pharmaceutical companies.

As inflation and interest rates rise, the future income streams these companies rely on become less certain (and less valuable).

Why does inflation matter to investors?

In 2022, COVID-19, natural disasters, and geopolitical tensions caused by the Russia-Ukraine conflict all negatively impacted global supply chains, causing inflation to rise rapidly in many countries around the world. This drove significant volatility in global stock markets, including the ASX.

As we've already discussed, inflation can also pressure certain share prices. Growth shares trade on expected future earnings. Analysts use financial models to discount these future cash flows to the present to calculate these shares' current value. As interest rates and inflation rise, so does the discount rate, which puts downward pressure on share price valuations.

Investors may seek to safeguard their portfolios by moving to safe-haven assets such as gold and value shares. This causes their prices to rise and the prices of growth shares to decline.

Gold is not a perfect inflation hedge, as it pays no dividends, but it has tended to hold its value over time. Value shares tend to be established businesses with strong current cash flows that are usually expected to grow at a slower (but more reliable) pace.

Gently does it

Gently rising inflation is generally seen as a positive for the share market, as it is consistent with the economy growing at a sustainable pace. Inflation above a certain level becomes problematic, although the impact differs depending on your investment style.

High inflation comes with higher interest costs, materials and labour costs, and reduced earnings growth expectations. The effects of inflation, however, are one of the key reasons to invest. As cash loses its value over time, you need to invest in some way if you want your money to retain (or grow) its purchasing power.

Investing in ASX shares can produce gains above the inflation rate, allowing investors to make money in real terms. Savings accounts may not keep pace with inflation in a low interest rate environment.

As an investor, the critical thing is to preserve the actual value of your money over time. Investing does not have to be complicated – a few ASX exchange-traded funds (ETFs) will do – but by not investing, you run the real risk of inflation eroding your purchasing power.

- Additional reporting by Motley Fool contributor Rhys Brock

Frequently Asked Questions

-

All sorts of different factors can drive rising prices. However, two of the most common types of inflation are 'demand-pull' inflation and 'cost-push' inflation. Demand-pull normally follows a period of low rates and high employment when households have significant disposable income and spend a lot of money in the economy. In this case, heightened demand causes the prices of goods and services in the economy to increase -- in other words, high demand pulls up the price of goods. In cost-push inflation, the price of raw materials (including labour) rises, increasing production costs. Producers eventually pass these cost increases to the end consumer, pushing up the prices of goods and services.

-

The main drivers behind Australia's persistently high inflation in 2023-2024 have been housing costs and the price of insurance and financial services. Ironically, the higher interest rates implemented by the RBA to fight inflation may contribute to higher costs across these two product groups. Other product categories, including transport and food, have also contributed to higher inflation in Australia recently. Goods and services in these categories are more exposed to energy prices, which have been particularly volatile given the current geopolitical tensions and conflicts involving major global oil producers.

-

The inflation rate in the March 2024 quarter was 3.6%. This is equal to the annual rate of change in the Consumer Price Index (CPI), the weighted average price of a basket of everyday household items. Although inflation has declined in 2023, it is still well above the RBA's target inflation, which is between 2% and 3%, meaning that prices may still increase faster than many people can afford. This means that cost of living pressures are starting to weigh on more households, potentially negatively impacting the quality of life for many Australians.