When it comes to ASX banking shares, Macquarie Group Ltd (ASX: MQG) isn't often bandied around with the same enthusiasm as something like Commonwealth Bank of Australia (ASX: CBA) or National Australia Bank Ltd (ASX: NAB). Sure, it doesn't have a current dividend yield north of 6%. Sure, it doesn't (usually) come with full franking credits attached for that maximum cash refund.

But I think Macquarie is a retiree's dream stock – and not just for the dividends.

If you were to read your typical 'top 3 stocks for retirees' column in your investing newsletter, names like CommBank, Alumina Limited (ASX: AWC) or maybe BHP Group Ltd (ASX: BHP) would be flying around. But I think there's more to a 'retiree's dream stock' or even the 'perfect dividend stock' than just yield. Remember, all of the big banks, along with BHP and most others cut their payouts substantially during the GFC in 2008/09.

Most 'high-yield' dividend stocks know how much their shareholders want juicy dividends, and so often pay out most of their earnings to accommodate this. For example, Westpac Banking Corp (ASX: WBC) currently offers a dividend yield of 6.57%, but does so by sending 81% of its earnings out the door in cash.

This is great for investors when the sun is shining, but when storm clouds gather, it's often a big cut in dividend payouts that serves as the company's umbrella. Not that Macquarie's dividends were completely safe during the GFC either – but more on that later.

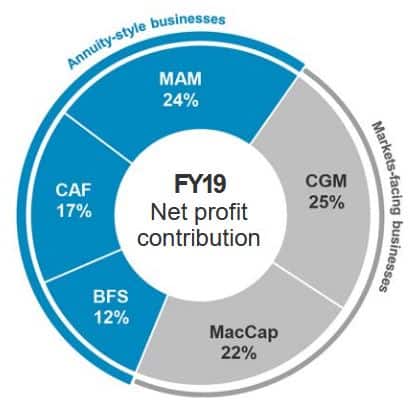

How does Macquarie earn its crust?

Macquarie is often labelled the 5th ASX bank, but as you're about to see, its not exactly a fair label. Sure, Macquarie offers mortgages, business banking, credit cards, savings accounts, personal loans, term deposits and even car loans… really anything you would go to a 'normal' bank for. But according to the company's 2019 financial year results, this arm of the business only contributed 12% of the company's total profits.

The remaining 88% hails from four other divisions of Macquarie, which are divided between "Annuity-Style Businesses" and "Markets-Facing Businesses", which are described in detail below:

Annuity-Style Businesses

Banking and Financial Services – as described above.

Macquarie Asset Management (MAM) – Contributes 24% of total profits

Macquarie is a global top 50 asset manager, providing a wide range of 'investment solutions' to clients. These include private wealth management as well as publicly available managed funds that cover everything from equity (shares), infrastructure and property to agriculture, private credit and fixed income.

According to Macquarie, MAM has around $543 billion of assets under management, which includes institutional capital from governments and pension and superannuation funds.

Corporate and Asset Finance (CAF) – Contributes 17% of total profits

CAF is Macquarie's large-scale lending division and focuses on corporate loans and infrastructure investment. Some examples of this work from the last financial year include loans to a major US telco to fund network developments and financing the smart meter rollout of the UK's largest energy supplier.

Markets-Facing Businesses

Commodities and Global Markets – Contributes 25% of total profits

Think of this division as investment services for large, wealthy clients (mainly institutional). Macquarie describes this service as providing clients with "an integrated, end-to-end offering (with) access to markets, financing, financial hedging, research and market analysis, and physical execution."

It's made up of eight subdivisions: cash equities, commodity markets and finance, credit markets, equity derivatives and trading, fixed income and currencies, futures, specialised and asset finance and 'central' (multi-divisional activities).

Macquarie Capital (MacCap) – Contributes 22% of total profits

This is Macquarie's 'investment banking' arm. It operates globally and provides 'capital solutions' to projects, ventures and other investments that the MacCap division sees as profitable from an investor standpoint. MacCap has a strong focus on infrastructure – particularly the energy space (both green and conventional).

But MacCap's presence can be seen closer to home too. You might be familiar with Wesfarmers Ltd (ASX: WES) and its 2018 demerger of the Coles Group Ltd (ASX: COL) supermarket network, but you probably don't know that it was MacCap that was the advising firm for this $19 billion spin-off. Ditto with the $3 billion merger of Fairfax Media and Nine Entertainment Co. Holdings Ltd (ASX: NEC) earlier this year.

This graph puts Macquarie's total profit base into perspective.

Source: Macquarie Group

As you can see, the annuity-style businesses and markets-facing businesses each contribute about half of Macquarie's total profits, but this wasn't always so. Until 2008, Macquarie was heavily weighted toward the 'markets-facing' side of the ledger, but when then-CEO Nicholas Moore took over the reins in May of that year, part of his vision for the company involved a move away from these lucrative but volatile earnings bases into the annuity-style divisions.

This was likely impacted by Macquarie's battering during the GFC, where the company slashed its dividend by 70% and saw its share price crash from more than $80 in November 2007 to less than $20 by February 2009.

Mr. Moore saw that an increased focus on a sturdier earnings base would be beneficial for the company and its shareholders – and this has proved true. Macquarie shares have since rebounded by more than 700% since the GFC, and dividends have been steadily rising since 2011.

So why is Macquarie the dream retiree's stock?

I think Macquarie is a retiree's dream stock not because it offers the most reliable dividend or the highest yield, but because of its unique ability amongst the ASX financials to provide a perfect cocktail of income and capital growth.

Not that it doesn't offer a decent dividend – on current prices its dividend is sitting at 4.57% (45% franked). I also like this dividend because it represents only 57% of the company's earnings – giving it a nice cushion against any market shocks (comparing very favourably to Westpac's 81% payout ratio). The company's refocused earnings strategy, centred on its annuity businesses will (in my opinion) ensure the company is far more prepared when the next recession rolls around and likely won't have to slash its payout by nearly as much as the GFC slicing.

Until then (and after), I think Macquarie is exactly the kind of company you'd want as a solid core of an income-focused retiree portfolio.

Foolish takeaway

Although I'm not yet a retiree, when that time comes around, I wouldn't want a portfolio consisting solely of tired, dividend-focused dinosaur companies. Sure, the other big banks, Coles and BHP are great sources of income and franking credits. But I hope to live a long, happy retirement and would want a star like Macquarie that can offer both long-term capital and income growth as a backbone of my income portfolio.