This morning international equities manager Platinum Asset Management Limited (ASX: PTM) posted a net profit of $102.2 million on revenues of $185.9 million for the six-month period ending December 31 2017. The profit and revenue were up 7% and 15% over the prior corresponding half.

The company will pay an interim dividend of 16 cents per share on 17.46 cents in earnings per share. This places it on a trailing yield of 4.5% plus the tax effective benefits of full franking credits.

The group also flagged that it had earned $20.8 million in performance fees over the period mainly from its "absolute" performance fee mandates. "Absolute" performance fee is generally fund manager jargon for funds that use gearing or have the capability to short stocks or use put or call options to hedge up or downside risks across specific holdings or markets.

In return for the more "active" nature of the asset management, clients are generally charged higher fees including performance fees.

In response to the fee pressure being exerted on fund managers by, inter alia, the popularity of index tracking ETF funds Platinum cut management fees across several of its funds in early 2017.

As at December 31 2017 Platinum had $27.1 billion in funds under management (FUM), which is 19% more than as at the same time last year. The growth in FUM is down to a mix of strong equity markets, investment performance, and net inflows of $0.9 billion.

Almost all of Platinum's funds had strong years in terms of investment returns and there's little doubt that it generally takes on more "sophisticated" investing strategies than the likes of peers Magellan Financial Group Ltd (ASX: MFG) and Perpetual Limited (ASX: PPT).

However, hedge funds generally have suffered a tough few years as quantative easing and virtual zero-interest rate policy (ZIRP) sucked volatility out of equity markets. Moreover, the gradual grind higher of US equities since 2012 has benefited traditional largely long-only U.S. focused asset managers like Magellan. This is because US markets have crushed the returns of other major European and Asian economies where Platinum likes to invest.

Still, Platinum's flagship international fund returned a mighty 25% in 2017 and averages a return of 17.9% over the past 5 years.

The group has plenty of investment expertise and might be a great place to work, but whether its scrip is a good investment is up for debate.

Just this morning its CEO and CEO in waiting team were on TV insisting that asset managers should focus solely on investment returns over operational asset gathering. That opinion is fair enough, but the two don't have to be mutually exclusive as Magellan has shown and Platinum is largely an exception to the rule in having little in-house focus on retail distribution or institutional business development that both fall under the "sales" umbrella.

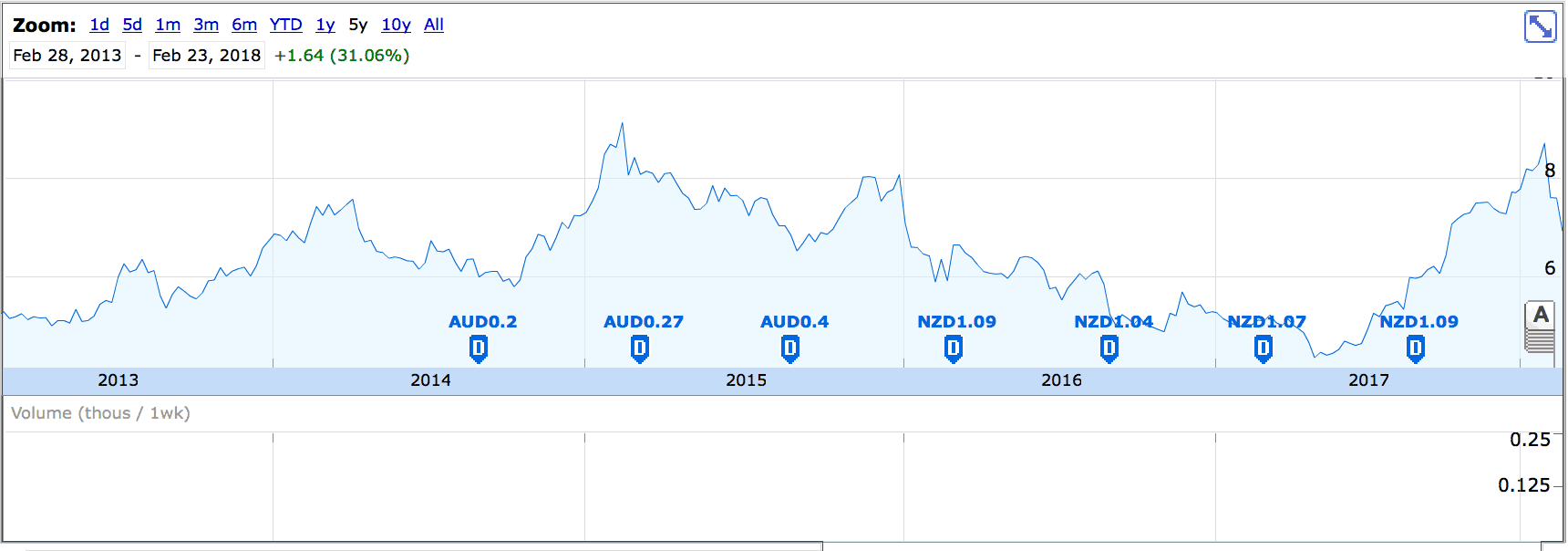

The stock's returns are also likely to loosely track the volatility of the group's investment returns given its lack of commitment to "asset gathering" as is shown by the chart below.

Chart: Platinum's volatile 5-years

The upside to the lack of commitment to creating a vertically integrated fund manager with a proper sales team is that costs are low and the business retains a lot of operating leverage as revenues should in theory rise faster than costs.

For example you can seed a $1 billion mandate generating fees at 1.3%pa into the international fund without the need to hire even one more staff member.

Platinum of course can also stay true to its mantra to solely being investment focused, but whether this is the right mantra for an asset manager looking to grow from $27 billion in assets under management is again up for debate.

Platinum also announced its founder and CEO, Kerr Neilson, would be leaving the role soon which may be adding to the downward pressure on shares that are 11% lower to $6.93.