- What’s so great about investing, anyway?

- 1. The power of compounding

- 2. Beating inflation

- 3. Building wealth over time

- 4. Additional income streams

- 5. Diversification for financial security

- Investment Strategy

- Broadening Your Portfolio

- Safety Assets

- Starting Your Investment Journey

- Example

- 6. Achieving financial goals

- Short-term Goals

- Long-term Goals

- Is it better to invest or save?

- Is investing mostly luck?

- Foolish takeaway

- Want to learn more about investing?

Interesting in investing? The Motley Fool has a wealth of articles covering all sorts of investing concepts and strategies. But none of this will mean much to you if you don't understand why you should invest in the first place.

So, in this article, we take a big step back and explain the many ways investing can help you achieve your financial goals.

Image source: Getty Images

What's so great about investing, anyway?

Here at the Fool, we are incredibly passionate about investing. We could talk about it for hours (and often do!).

There's nothing we love more than getting into lengthy debates about the merits of value investing versus growth investing, whether cryptocurrencies are worth the risk, or the best defensive shares to buy when interest rates are high.

But sometimes, we must remember to start by explaining exactly why investing is so amazing in the first place – and why we think everyone should be doing it!

So, here we'll cover some of the key benefits of investing – like how compound returns can help you grow your long-term wealth (without you having to do anything) or how the passive income you make from dividends can help supplement your income (and might even allow you to work less).

Because we think that once you know about the many benefits investing provides, you'll be just as passionate about it as we are!

1. The power of compounding

Essentially, compounding means that you earn interest on your interest. While it might not sound all that impressive, it's one of the most powerful concepts in investing. Einstein even called compounding the eighth wonder of the world!

The way compounding works is pretty simple. Let's say you have an investment that pays interest (or a dividend) every six months. When you receive the payment, you can withdraw it as cash or reinvest it into the same investment.

Reinvesting it adds to the principal and, therefore, grows the next interest payment you receive. It means the amount received will be slightly higher each time. If you continually repeat this process over time, a snowball effect is created whereby the interest you receive grows exponentially.

Here's a quick example to illustrate the magic of compounding.

Assume you have two investors, Ralph and Lisa. Each has a $1,000 portfolio that pays roughly 5% annual interest, payable every six months. Each can choose whether to take or reinvest the money when they receive payment.

Ralph uses his portfolio to supplement his income and accepts his payment as cash every six months. On the other hand, Lisa isn't concerned with earning additional income and instead wants to grow her wealth over the long term. So, she decides to reinvest all her payments.

Fast forward ten years. The total value of Ralph's payments over the period was $500, comprising 20 half-yearly payments of $25. However, Lisa's portfolio has increased in value over the same timeframe from $1,000 to $1,638.62. If she cashes out her portfolio now, she would have made $138.62 more than Ralph simply by reinvesting her payments into her portfolio and harnessing the power of compound interest.

Now, imagine if instead of Lisa's $1,000, it's your lifetime's worth of savings; instead of ten years, it was your entire working life. The wealth-generating potential of compounding can quickly become quite astonishing – it might even end up paying for your retirement!

2. Beating inflation

Inflation occurs when the prices of goods and services increase over time.

Even the healthiest of economies have low inflation levels. It's unavoidable. It just means that the economy's demand for goods and services is strong, and people are spending money.

So long as the central bank keeps inflation within an acceptable band (about 2% to 3% per annum), everything is hunky dory. The economy is growing, but wage increases keep pace with price increases.

Still, even if we begrudgingly accept that a low level of inflation is a healthy thing for an economy, it doesn't provide us with much comfort when we get to the checkout and realise our groceries cost more than they used to.

Economists refer to this as an erosion in our 'purchasing power'. In other words, the same amount doesn't buy as much stuff as it used to.

So, while you might think you're saving for the future by squirrelling away your money in your everyday bank account (likely earning next to nothing in interest), its real value could be declining – especially when inflation is high.

But what if, instead of saving your money, you invested it?

Investing your money in a diversified portfolio of financial assets can be a great way to beat inflation and grow your real wealth over time.

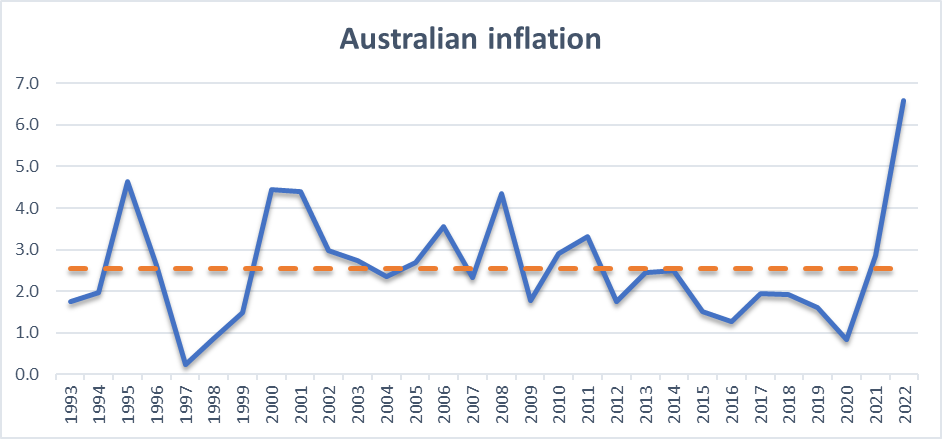

For example, see the below chart of Australia's annual inflation rate over the past 30 years. While inflation has been volatile (and spiked recently), the average rate over the past 30 years (represented by the red dotted line) has only been about 2.6%.

Compare this against the S&P/ASX All Ordinaries Index (ASX: XAO), which has returned, on average, about 9.2% each year over the same period1. This shows that a well-diversified portfolio of Australian shares would likely have delivered a return well above the inflation rate.

Data source: The World Bank

3. Building wealth over time

A key ingredient in every successful investment portfolio is time.

Here at the Fool, we don't believe in get-rich-quick schemes. We believe the best way to grow your wealth over time is by investing your money in quality shares and other financial assets. But this requires a long-term mindset.

As mentioned, the average annual return of the ASX All Ords has been about 9.2% over the past 30 years. But that's just the average – sprinkled in were some terrible years, too.

For example, there was the dot-com crash in 2000, then the bear market caused by the Global Financial Crisis (GFC) in 2007. And, of course, as recently as 2020, the COVID market crash took its toll.

Short-term investors who panicked and sold their shares in one of those bad years could have suffered massive losses – but longer-term investors who rode out those short-term downturns would have been rewarded with a long-term average return.

Investing requires discipline and patience (and sometimes even nerves of steel!).

Set clear goals and have a firm idea of what you hope to get from your investments – be it a financially secure retirement, savings for a holiday, or your child's education. Whatever your long-term goals are, if you can easily visualise them, it will help you stick to your plans when things get a little rocky.

4. Additional income streams

As discussed earlier, your investments can provide regular income streams – from interest, dividends, or other cash distributions.

In our earlier example with Ralph and Lisa, we explained how Lisa reinvested her regular distributions to harness the wealth-generating power of compound interest. However, Ralph elected to take his payments as cash to earn a passive income stream.

As illustrated, reinvesting your interest will typically provide better long-term returns, thanks to compounding. But taking these payments as cash can still offer other important advantages.

For example, additional income from your investments might allow you to work less and pursue other passions. This might be just as important to you as long-term wealth.

And, as you get older, these payments will help finance your lifestyle in retirement.

So, depending on your stage in life and your personal investing goals, the ability of your portfolio to earn a steady stream of passive income can be precious.

5. Diversification for financial security

Diversifying your investments is essential for managing portfolio risk. As the saying goes, "Don't put all your eggs in one basket." If you concentrate all your resources in one place and it falters, you risk losing everything. By spreading your investments, you protect yourself from such scenarios.

Investment Strategy

Investing all your money in a single stock is risky because it ties your financial success solely to that stock's performance. Instead, diversify by investing in multiple stocks. This way, your overall portfolio can continue to grow even if certain stocks don't perform well.

Broadening Your Portfolio

Diversification isn't limited to stocks; you can widen your portfolio by including various financial assets such as:

Each type of asset has its own risk and return profile, which can help stabilize your portfolio through different market conditions.

Safety Assets

Assets like bonds and gold are considered safe-haven investments, particularly useful during economic downturns. Having part of your portfolio in these assets can help offset losses from stocks, which are often more affected by recessions.

Starting Your Investment Journey

If you're new to investing, exchange-traded funds (ETFs) offer a cost-effective way to diversify your portfolio. ETFs trade like regular shares and can give you broad exposure to various assets.

Example

The iShares Core S&P/ASX 200 ETF (ASX: IOZ) provides a practical example. This ETF invests in the top 200 shares on the ASX by market capitalization, allowing you to buy into a diversified portfolio with a single transaction. By doing so, the fund aims to reflect the broader ASX200 Index performance, making it an efficient choice for investors seeking diversity without complex portfolio management.

6. Achieving financial goals

Setting a clear set of financial goals is crucial for maintaining motivation throughout your investing journey. It provides personal accountability and a clear sense of purpose. One of the key benefits of investing is the ability to tailor a portfolio to meet specific goals.

For short-term goals—like purchasing fancy clothes or planning a weekend getaway—you might prefer lower-risk investments such as bonds or high-interest savings accounts. These options are usually liquid, stable, and provide some income without significant price declines.

For long-term goals, such as buying a home or securing a comfortable retirement, you can consider allocating more funds to riskier assets like shares. Although these assets can be volatile in the short term, they generally offer better returns over the long haul.

Short-term Goals

- Options: Bonds, high-interest savings accounts

- Characteristics: Low-risk, liquid, income-generating

Long-term Goals

- Options: Shares, diversified portfolios

- Characteristics: Higher risk, potentially more volatile but better long-term returns

We encourage you to read our article on setting financial goals before you start out on your investing journey (though it can still help seasoned investors, too!). Setting reasonable goals at the outset is the best way to set yourself up for investing success.

Is it better to invest or save?

The choice between saving and investing depends on your financial goals and risk tolerance; savings offer security and liquidity for short-term needs, while investing provides potential for higher long-term growth but involves more risk. Ideally, a balanced approach combining both strategies ensures you have access to funds when needed while working towards substantial long-term financial growth.

Is investing mostly luck?

Investing is not mostly luck; it relies on research, strategy, and understanding market dynamics. While there is certainly an element of unpredictability due to market fluctuations, informed decision-making and a well-diversified portfolio can mitigate risks. Consistent, long-term investing often yields results based on the principles of compounding and market trends rather than sheer luck.

Foolish takeaway

In this article, we've highlighted a few good reasons why everyone should start investing. The list is not exhaustive – you may be able to think of even more advantages to investing.

And if you're inspired to start, we can provide you with plenty of the tools and tricks required to become a successful investor. Happy investing!

Want to learn more about investing?

You've come to the right place!

This article is part of Motley Fool Australia's comprehensive Investing Education series, covering everything from budgeting and saving to basic investing concepts and how much money you'll need to start.

Packed with easy-to-understand and regularly updated information, our articles contain the answers to your most frequently asked questions about share market investing.

Motley Fool's Education series is tailored for beginner and experienced investors alike and also includes helpful tools and resources, an A-Z glossary of Investing Definitions, and guides to specific topics of interest, including retirement planning, gold and property investment.

- To read the previous article, go to What is investing?

- Check out the next article, Investing versus saving