S&P/ASX 300 Index (ASX: XKO) share Nick Scali Limited (ASX: NCK) is a company that I am getting closer to investing in.

Don't get me wrong, I believe Nick Scali is going to report a sizeable decline in profit in FY24 due to the effects of higher interest rates and, with that, the higher cost of living. But I'd suggest the current Nick Scali share price is taking that into account.

Image source: Getty Images

Much better Nick Scali share price valuation

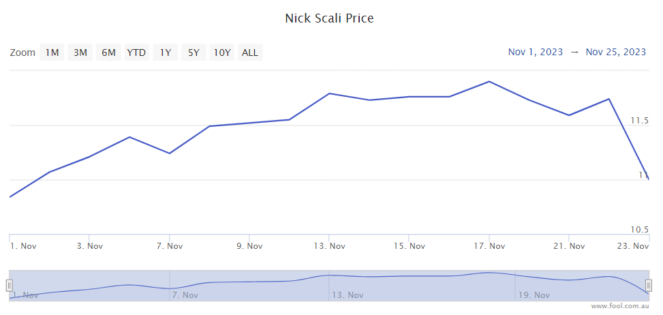

As we can see on the chart below, the Nick Scali share price is down 10% from 16 November 2023 and down 33% from November 2021.

I think discretionary retailers like Nick Scali will see demand go through cycles. Sometimes demand is weaker and sometimes it's stronger. I believe the best time to buy into retailers like this is when retail conditions are deteriorating and the outlook is weak for the foreseeable future.

Certainly, we shouldn't expect Nick Scali to generate as much profit as it did in FY23 for some time. Those numbers could be attributed to the effects of the COVID-related retail boom. The ASX 300 share is currently valued at under nine times FY23's earnings.

If we look at the possible profit for FY24, the earnings per share (EPS) could be 92.2 cents, according to the projection on CMC Markets. That would put the Nick Scali share price at under 12 times FY24's estimated earnings.

The recent sell-off of the ASX 300 share was sparked by the sale of a significant chunk (4.6 million) of Nick Scali shares by boss Anthony Scali. However, he still owns 6.4 million Nick Scali shares, so Anthony Scali is still the largest shareholder and owns around 8% of the business.

Is bad news on the way? I wouldn't be surprised to see a deterioration in demand for furniture in the next few months. But the Nick Scali share price won't necessarily move down at the same pace as the weakening conditions. Perhaps it may not fall at all.

If the Nick Scali share price does keep falling, I think this would provide an even better margin of safety for purchasing shares. I'd prefer to invest at a Nick Scali share price of below $10. The company opens this trading week at $10.67 a share.

That said, I don't need to buy at the absolute bottom for the Nick Scali share price to do well in the long term. Perhaps we may have already seen the bottom in the share price when it dropped below $8 in 2022.

Until the retail outlook improves, we can collect good dividends on Nick Scali shares in the meantime. According to the estimate on CMC Markets, the grossed-up dividend yield could be 7.4% in FY24 at the current valuation. If the Nick Scali share price falls further, that could mean an even stronger dividend yield.

Why I'm confident about the future

I believe there are a number of drivers that can help earnings and, ultimately, the Nick Scali share price in the long term.

Australia's rapidly growing population is certainly a tailwind because it means more potential customers and more possible locations for stores.

At the end of FY23, the company had 64 Nick Scali stores, with a long-term target of 86. For its recently-acquired Plush business, there were 43 stores at the end of June 2023 and it wants to grow this network to between 90 to 100 stores.

The ASX 300 share can also generate good profit margins from its online sales, which are currently small.

Management has also talked about expanding to the UK, which could open up a good growth avenue.

I also like that the business is steadily building up a portfolio of land holdings around the country. This gives it more security in securing good retail locations and allows it to have more control of costs. It also builds an asset base. From FY25 onwards, the strategy may lead to capital growth in the value of the land if commercial land prices stop falling by the end of FY24.