Telstra shares have outperformed the S&P/ASX 200 Index (ASX: XJO) in the year to date.

The telco's share price has delivered an exceptional 6% return since the start of the year. By comparison, the benchmark ASX index is barely keeping its head above water so far in 2023, up by 0.3%.

Telstra is the top communications share by market capitalisation on the ASX and has long been a reliable blue-chip share. However, over the past month, Telstra shares have traded sideways, closing at $4.19 a share on Thursday.

So is now the time to pounce on the telco behemoth, or could there be trouble ahead?

Let's take a look at what two Foolish team members had to say about the bull and bear case for Telstra shares.

Image source: Getty Images

The bull case for Telstra shares

By Monica O'Shea: I am long-term bullish on Telstra shares based on multiple strengths.

Firstly, Telstra appears to be focused heavily on growth and making progress on its T25 strategy. On the network side, Telstra's 5G network is the largest in Australia and covers 81% of the population, close to the company's FY23 target of 85% of the population.

Telstra's CEO Vicki Brady sees the mobile business as central to the company's T25 growth. Further, Telstra's InfraCo assets may deliver value for shareholders in the future, some experts predict. Infraco could be worth about $22 to $23 billion, according to Goldman Sachs.

Secondly, Telstra shares could be trading at a discount if analysts are correct. High-profile brokers, including Goldman Sachs, see significant growth in the telco's share price. Goldman has a buy rating on Telstra with a $4.60 price target, while Morgans can see Telstra shares reaching $4.70.

Thirdly, Telstra's half-year results were solid on a number of key metrics. In 1H23, Telstra's earnings before interest, taxes, depreciation and amortisation (EBITDA) soared 11.4% and total income grew 6.8%. Telstra's net profit after tax (NPAT) lifted 25.7% in 1H23 compared to the prior corresponding half. This could bode well for the future.

Fourthly, the Telstra dividend is extremely reliable and, in fact, has increased in the past year. Telstra maintained its dividend during COVID and this year lifted its interim dividend to 8.5 cents per year, 6.25% more than the prior corresponding half. Telstra also delivered an 8.5 cents per share final dividend last year.

Overall, I see the Telstra share price as a safe share to invest in over the long term.

The bear at the other end of the line

By Mitchell Lawler: I want to provide a caveat to my bearish stance before we get underway. Telstra, as a business, is rather impressive. The service it provides to Australians, particularly in regional and remote areas, is unrivalled. However, there are plenty of 'impressive' companies that fail to have the makings of an outperforming investment.

One of my main gripes with Telstra is that the real crown jewel of the company is its mobile network. The rest of the business – including Fixed and InfraCo – offers marginal growth, if not erosion, to the company's EBITDA.

There is a chance that management will look to sell off these less-performing assets to unshackle what looks to be an anchor. Personally, I believe that would be a step in the right direction for Telstra shares — pivoting toward a higher growth area of telecommunications.

In saying that, the mobile segment is not without its drawbacks. After TPG's merger with Vodafone Hutchinson Australia, there are now two formidable competitors (TPG Telecom Ltd (ASX: TPG) and Optus) to Telstra's market dominance.

As we all know, the mobile industry does not stand still – 2G, 3G, 4G, 5G. I believe each generation of new technology poses an execution risk for Telstra, which will be more prominent in the future now with well-capitalised competition.

At the end of the day, Telstra's moat is its infrastructure and the enormous capital required to replicate it. Though, with time, I'm not sure this moat will be as wide as management and shareholders had hoped.

Already we can see the Australian telco giant is attempting to stave off encroachment by offering an 'olive branch' to TPG through a 10-year network-sharing arrangement. This would have made TPG reliant on Telstra and inserted a hefty gap in Telstra's infrastructure lead, but the proposal has been thrown out by the competition watchdog.

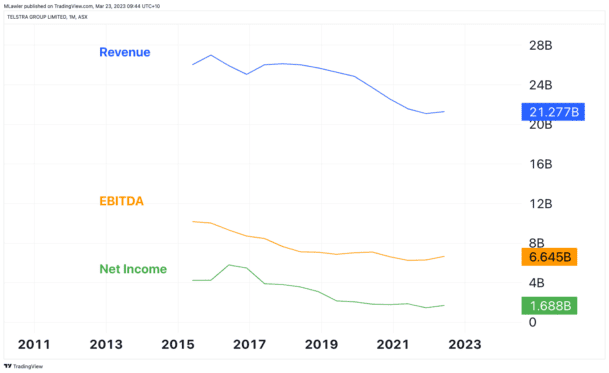

If the competition is willing to play the long game, investing in their own infra, I think we could see Telstra's mobile business decline in the same way its broadband business has over the years, demonstrated by the chart above.

Given these risks, a price-to-earnings (P/E) ratio of around 26 times on Telstra shares is a tad too rich to be palatable in my opinion.