Wesfarmers Ltd (ASX: WES) shares are not cheap, relatively speaking or in absolute terms, but you must be doing something, right?

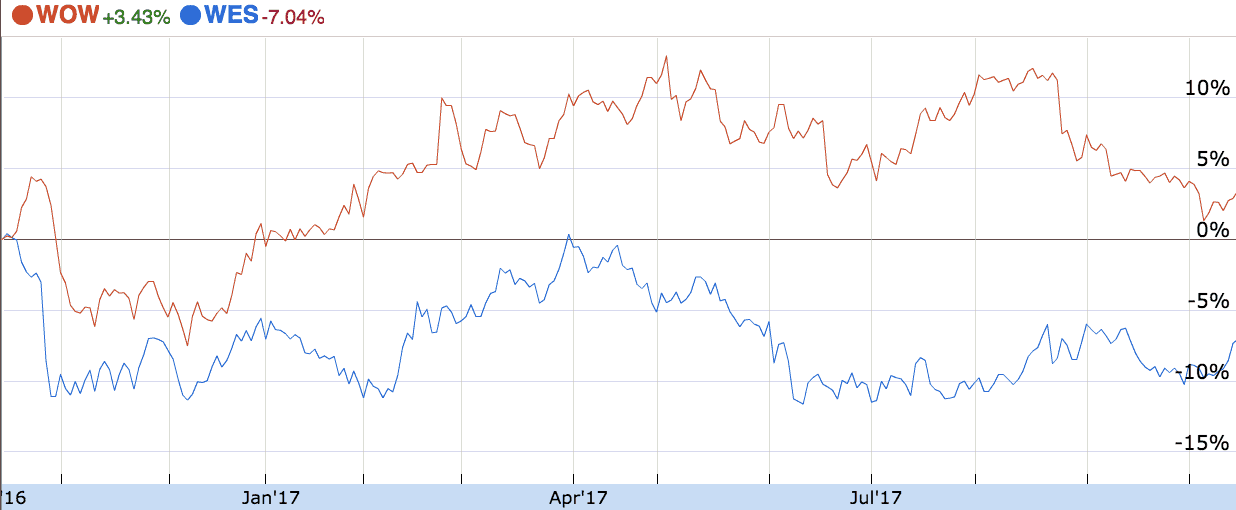

Wesfarmers V. Woolworths Limited (ASX: WOW)

Wesfarmers is Australia's leading retailer, owning Coles, Kmart, Bunnings Warehouse, Target and Officeworks, amongst other things.

Taking a look at the chart above, you might think that given its decline over the past year Wesfarmers shares may now be compelling value.

One way analysts and investors determine a valuation is to use 'relative valuation'. They will use a ratio or figure, such as the price-earnings ratio (P/E), price-to-book ratio (P/B) or dividend yield, and compare the result to that of its peers, or contrast it with a historical average.

If the analyst is a little savvier they might use the 'Enterprise Value (EV) to Earnings Before Interest, Taxes, Depreciation and Amortisation (EBITDA)' ratio. Don't be overawed, it's not difficult to calculate.

In fact, sources like The Wall Street Journal do it for you.

According to WSJ, Wesfarmers has an EV/EBITDA ratio of 10.4 times, whereas Woolworths shares trade at 10.3 times. Lower means cheaper.

But, before you compare them side-by-side you need to consider what goes into the EBITDA figure. Wesfarmers' results have been boosted by growth in Bunnings, coal prices and a dominating Kmart. It has been weighed down by Target.

Therefore, that EV/EBITDA figure is only reliable if the results are sustainable.

According to some analysts, Wesfarmers' EBITDA will continue to grow modestly in the years ahead, led by Bunnings.

So if modest growth is what we can expect going forward we shouldn't pay too much for the shares, right? In other words, we should pay a price which justifies this lower-than-ideal growth rate.

According to my analysis, Wesfarmers' global peer group's average EV/EBITDA is around 8 times. Now, that's global figures — and Australia is Australia. But even with a modest local premium, Wesfarmers shares are not a bargain.

Now, in absolute terms, according to my analysis, Wesfarmers' shares appear to be modestly overvalued.

Absolute valuation is more reliable than relative valuation, in my opinion, but it is harder to explain without going into detail.

But is it a buy?

One big problem with professional investors is that they have mandates to be invested. Meaning, even if they don't have any great investments in mind they will buy good or — worse still — mediocre investments because they need to be 'invested'.

You and me, on the other hand, don't need to do anything. We can reserve our portfolios for great investment opportunities – nothing less.

Therefore, while I think Wesfarmers is a great company and it is likely to go higher over the long-term, I'm not buying its shares for my portfolio.