A lot of retail investors will often hear professional investors talk about a company's return on equity being low or high and what this means for it as an investment prospect.

However, return on equity as an investing metric often confuses investors due to its complicated definition, the different inputs involved in calculating it, and other factors like how a company's leverage may impact return on equity's worth as an investing metric.

For the record Investopedia defines return on equity as "a measure of financial performance calculated by dividing net income by shareholders' equity. Because shareholders' equity is equal to a company's assets minus its debt, ROE could be thought of as the return on net assets."

However, it's importance as an investing metric often bypasses retail investors because they're unclear on what it demonstrates.

In order to help, I'll use calculating return on equity on an investment property as a simple example to show why this is such an important investing metric.

Let's assume you can buy an investment property "A' for $1 million with a $100,000 deposit and that property yields net rent of $20,o00 per year. The property's return on equity is 20% as $20,000 / $100,000.

Let's assume another investment property "B' is bought with the same deposit for the same amount and yields just $10,000 per year in rent. Its return on equity is just 10%. And both properties were bought with $900,000 leverage on an LVR of 90%. The 'equity in the property is the $1 million assets – the debt of $900,000 to equal the $100,000 equity or deposit.

We can see that property A is a much more profitable asset to own, with an ROE of 20%. Put simply the more free cash flow an asset can make on the less investment into it the more profitable it is and the more likely it is to rise in value especially if that free cash flow increases strongly (either via rent increases or bigger company profits) over time. After all if properties A and B went to auction tomorrow, property A would definitely get bid up higher.

We can also see that companies with no debt and high returns on equity should be especially profitable as debt can mislead or distort return on equity. For example if property B was funded with less debt of say $800,000 to create equity of $200,000 its ROE would actually be lower at 5%, but the property is less leveraged to incur lower interest payments on the debt.

So let's take a look at two companies with no debt that post very high returns on equity to suggest shares in these companies are potentially very good buys.

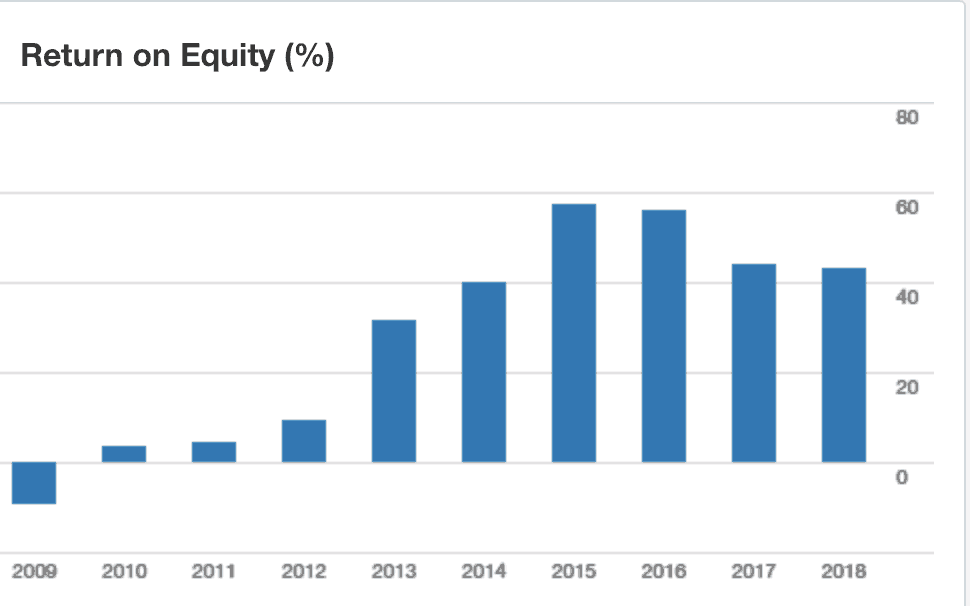

Magellan Financial Group Ltd (ASX: MFG) had no debt and cash or cash equivalent assets on hand of $451 million as at December 31, 2019. It also has a low cost base and is scarily profitable. Check out its FY13-FY18 return on equity below.

Source: Commsec, July 4, 2019.

Source: Commsec, July 4, 2019.

We can see that Magellan has boasted a ROE above 40% since FY 2014. That's sensational and a good guide as to why the shares are up around 5x over the period. Why buy an investment property with strata fees and noisy tenants when you could buy an asset like this? You won't find an investment property with an ROE anywhere close to 40% and you won't be able to buy it for transaction fees as low as $9.95!

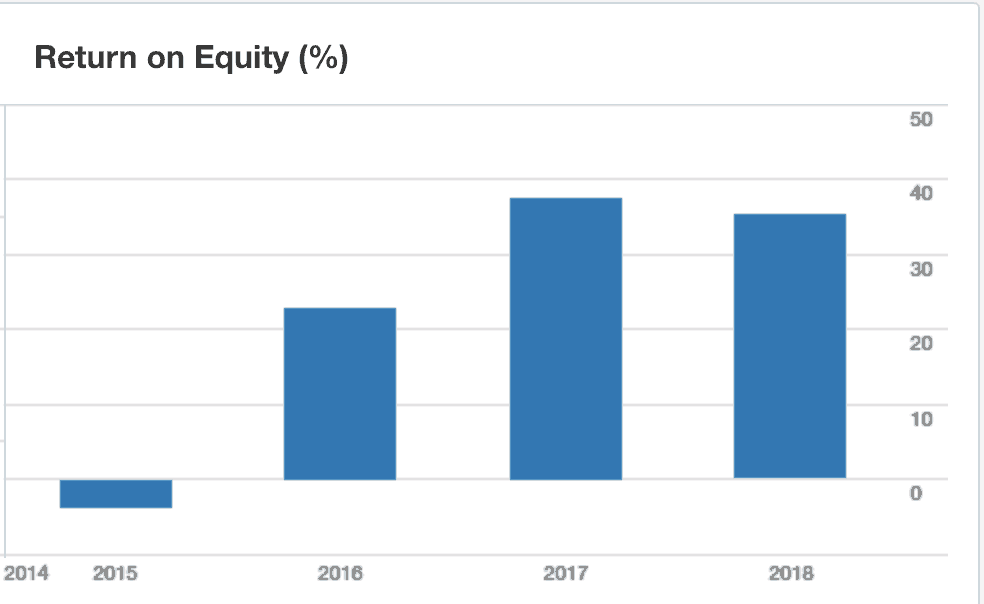

The a2 Milk Company Ltd (ASX: A2M) had no debt and NZ$288 million cash on hand as at December 31, 2019 and is a stock I recently bought again myself. It's growing its free cash flow at very strong rates thanks to the growing popularity of its a2-only-protein baby formula and supermarket milk in China, ANZ and the U.S. Let's take a look at its ROE from 2015 to 2018.

Source Commsec, July 4, 2019.

We can see that a2's return on equity is getting towards a very high 40% despite the group investing heavily in sales and marketing to grow its business in the US and China. No surprise shares in this highly profitable asset have climbed from $1.60 in January 2016 to $14.48 today. I expect they could go higher.

Outlook

So now we can see why investors love shares in companies with a high return on equity and no debt as buying these shares means you're buying very profitable assets.

That's before we even remember that debt is generally a share price sinker that most companies should avoid.

The worth of a high return on equity is no big secret, but you'd be surprised how the majority of investors still buy shares in low quality companies for reasons usually related to the fact that they consider these companies cheaper or better value.

Other companies that I've regularly covered with a high return on equity, but significant debt include REA Group Limited (ASX: REA) and CSL Limited (ASX: CSL). These two businesses have also been share market stars over the past decade and are worth owning at the right price in my opinion.