The falling housing market isn't worrying Mirvac Group (ASX: MGR) with the property developer brushing aside concerns in its bullish quarterly update although its share price reaction tells a different story.

The stock had initially jumped higher before giving up gains to end flat at $2.25 on Tuesday after management reiterated its earnings per share (EPS) and dividend growth targets as it touted the strong performance of its office and industrial property business.

I don't think that's enough to make the stock a buy, not when the headwinds in its residential business are growing, and UBS has even gone a step further to warn that the stock is likely to face a consensus profit downgrade in the not too distant future.

"Office and industrial fundamentals remained rock solid, but residential activity continues to soften. Mirvac omitted the usual breakout of major residential EBIT [earnings before interest and tax] contributors, so while individual Q1 project sales rates are unknown, the total number of lots released fell (428 Q1 versus 550 pcp)," said UBS.

"We continue to believe the residential market will be the marginal driver of MGR's relative performance and housing activity is falling ahead of expectations and not reflected in FY20+ consensus estimates (UBSe 7% below consensus in FY20)."

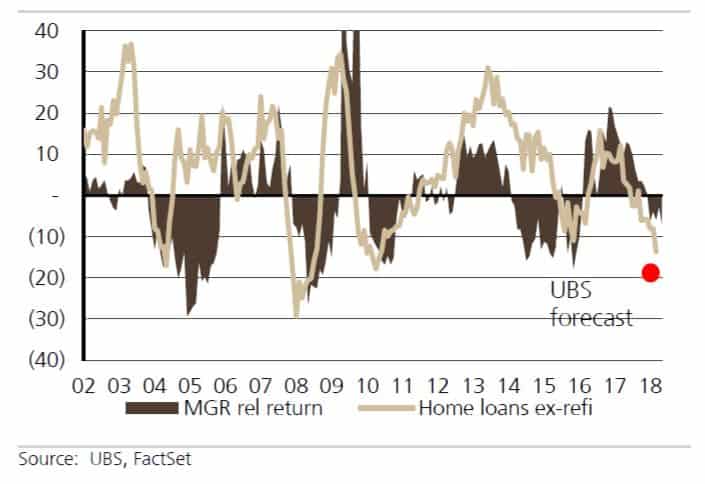

What's interesting is that UBS found a correlation between Mirvac's relative return and home loan growth (excluding refinance). Credit growth is slowing and most experts believe it will fall further as house prices come under increasing pressure.

Going Down: Mirvac relative performance vs. home loan growth (%)

Mirvac isn't the only one that will hurt from this trend as its peers Stockland Corporation Ltd (ASX: SGP) and Lendlease Group (ASX: LLC) will also feel the pinch.

However, I think Mirvac is particularly sensitive to this housing downturn given its exposure to the Sydney apartment market – an area particularly hard hit from the withdrawal of property investors.

What's more, the stock is trading at what I consider to be a full valuation. Mirvac is on an FY19 consensus price-earnings (P/E) multiple of nearly 14 times. That's near the top of its five-year average P/E band.

The company's FY19 outlook might still look stable enough but the risks lie in FY20.

UBS has a "sell" recommendation on the stock with a price target of $2.22 a share.

If you are looking for blue-chips that are better placed to outperform the S&P/ASX 200 (Index:^AXJO) (ASX: XJO) index, you might want to read this report from the experts at the Motley Fool.

They've picked their best three blue-chip stocks for FY19 and you can find out what they are by clicking on the free link below.