Retail entrepreneur Dick Smith recently announced that he's to close his line of own brand foods sold in the supermarkets of Woolworths Limited (ASX: WOW) and Wesfarmers Ltd (ASX: WES) because he can't compete with the margin crunch brought about Aldi.

According to the Fairfax Media Limited (ASX: FXJ), Smith complained that Aldi was "unbeatable" on price thanks to its low-cost business model of no floor staff, minimal checkout staff, and no plastic-bag-like freebies. Aldi shoppers cannot use self-serve checkouts as they are known to add to a supermarket's costs because of the amount of food stolen via them. The German discounter also has a limited range of foodstuffs and sources all its foods from cheap overseas producers.

However, most important is the fact it operates as a private company, which means it does not bow to shareholder pressure over its strategy of gaining market share at the expense of short-term profits or dividends.

As such Aldi and other low-cost operators now entering Australia such as Costco and Lidl have a similar business model to Amazon. Inc. in sacrificing profit margins to take competitors' market share.

Notably, Costco also employs a members only shopping scheme in a similar way to Amazon Prime.

The margin sacrificing business model can work for companies like Amazon or Lidl as equity owners don't demand free cash flow be returned in dividends, but would rather see it reinvested in expansion or attracting shoppers by the ability to sustain lower margins.

The worse news of all for shareholders in Woolworths and Coles is that this former supermarket duopoly still have some of the highest profit margins in the world to be eroded.

No wonder Wesfarmers' management decided the time is right to sell off its cash-generating machine in Coles via an upcoming IPO.

In retail profit margins are key, and if the retail company you hold shares in is likely to be under long-term margin pressure I'd suggest following the lead of Wesfarmers' management and selling your shares now while the going is reasonably good.

The combination of falling margins and steadily eroding market share is bad for any business and a traditional 'sell signal' for professional investors, with broker CLSA reportedly downgrading Woolies and Wesfarmers shares to a "sell" this week.

The kicker is both these businesses are already on rich profit multiples and I expect they'll offer investors nothing but sideways returns at best over the decade ahead.

For example, Aldi and Lidl entered the United Kingdom's more competitive supermarket sector from 1990 and now reportedly account for £1 in every £8 spent in UK supermarkets, with the victims of this disruption being the incumbent supermarkets.

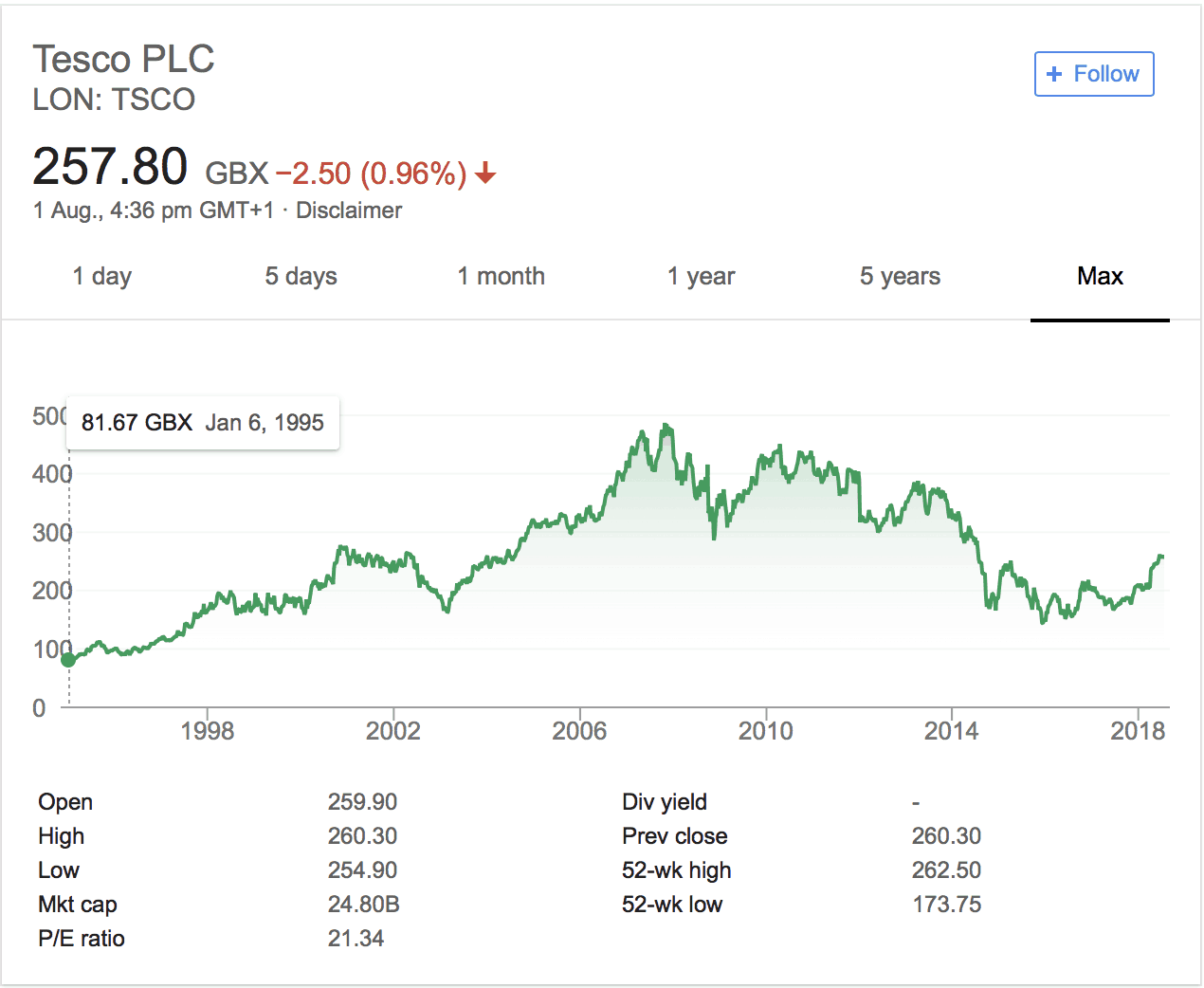

Take a look at the share price chart of the UK's leading supermarket Tesco plc below. In the early-2000's Tesco was widely believed to have an impregnable market position by virtue of its scale, but you can see how its share price has gone NOWHERE for nearly 20 years now!

Source: Google Finance

If you want your shares to go nowhere over the next 20 years while you collect some dividends then the supermarket space might be for you, but if you want to build serious share market wealth for yourself then you've got to look to tomorrow's blue chips….