Shares in asset manager and investment bank Macquarie Group Ltd (ASX: MQG) hit a record high of $123.99 this morning as investors bid the stock up as the Australian dollar weakens versus the U.S. dollar.

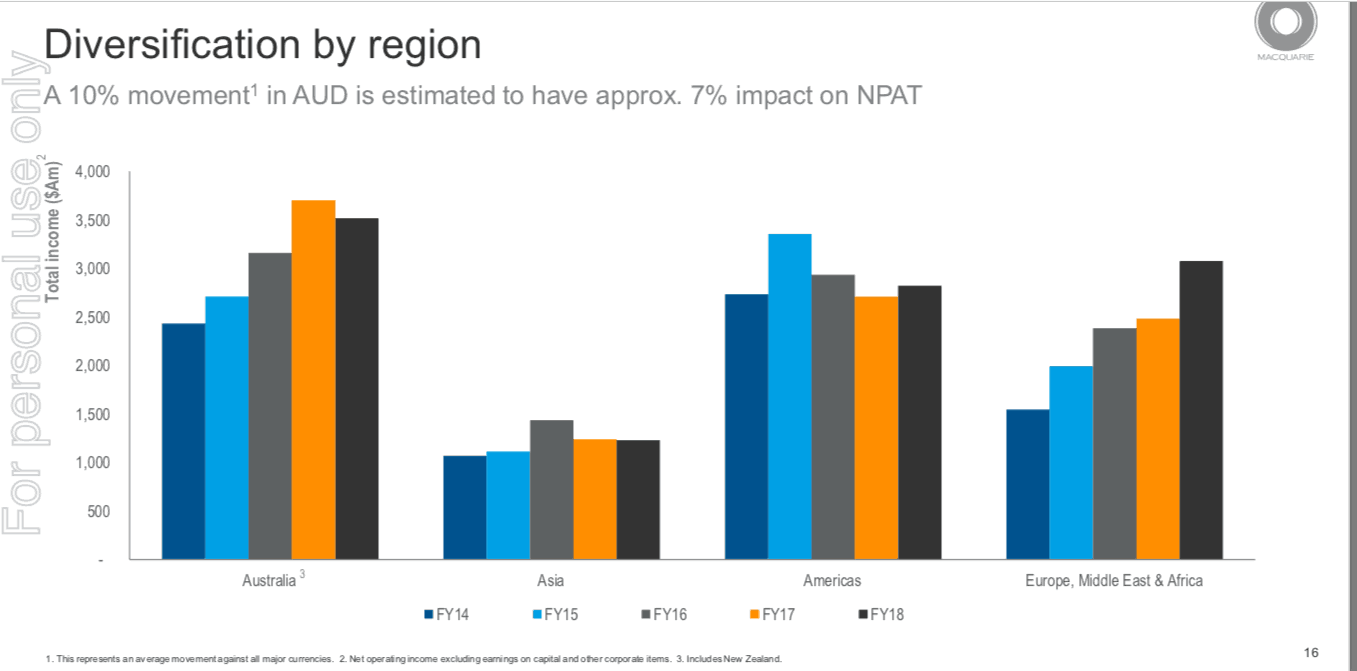

On reporting its full year results in May 2018 the bankers flagged that every 10% movement in the Aussie dollar would impact net profit by 7% (see below chart), with the falling dollar leading investors to re-rate Macquarie's earnings outlook for 2018.

Source: Macquarie Group FY18 Presentation

It's not just the falling dollar sending Macquarie shares higher though as the U.S. economy has delivered robust growth, while the above chart shows how European income growth was the star performer in FY 2018.

Macquarie also now earns around 70% of its profits from what it describes as "annuity style" businesses in that they are in the asset management or corporate financing (lending) space and should earn reliable fees regardless of activity or confidence levels in the wider capital markets.

Notably, its capital markets-facing businesses should benefit from more volatility in 2018, after 2017 was characterised by eerily-low asset price volatility on the back of quantitive easing, among other factors.

It's common sense that capital-market facing businesses like brokerages and M&A advisory functions do better when capital market activity is stronger (after a weak 2017) and I expect these businesses to perform better in the years ahead.

Macquarie the eco warrior?

Moreover, Macquarie is also turning itself into something of a shock "eco-warrior" via its heavy investments into green and renewable energy or infrastructure projects.

In 2017 the bankers even spent around $4 billion buying the Green Investment Bank (GIB) off the UK government to provide a vehicle to really ramp up its green investments.

In effect the GIB is a modern-day successor to the public-private-partnership multi-lateral development banks of old (think World Bank, African Development Bank) largely setup to promote private enterprise (via lending) into emerging markets at profitable rates of return.

So have the Mac bankers given up their bonus culture and long hours to bang the bongos, develop a deep social conscience and commit to environmental protection?

You've got to be kidding!

Macquarie pulled out all the stops to buy the GIB as it sees the long-term profit spinning potential in using it as an investment vehicle sitting in the widening sweet spot of syndicated green lending in partnership with super-sized investors.

In fact in today's world many sovereign wealth, charity, or other quasi-public investment funds are often mandated to seek out green investment opportunities and this trend is likely to accelerate over the long term.

Macquarie is already a well established infrastructure investment expert with wide deal making and advisory competencies in lending, debt, or asset financing. The GIB deal widens its connections, distribution networks and universe of investment opportunities.

The bankers probably see an opportunity to generate a greater return on GIB's current assets and lending activities going forward, while being able to source funds (liabilities) from a cashed up queue of public and private capital backers at relatively cheap rates.

Just last week it announced a cash raising of around $3.5 billion in debt via syndicated lending facilities with big-hitting banking partners like HSBC in Asia. Of the $3.5 billion raised it's already earmarked around $1 billion (£500m) to finance green investments.

If Macquarie can crank the GIB's profitability (which would be no surprise), while growing its balance sheet due to the queue of partners and available investment projects its acquisition is likely to be earnings per share accretive over the long term.

Furthermore, now it has full control of the GIB it has the option to sell off some investments at a potential profit (the asset stripping allegations that have reared up in the past) and to cut costs via potential staff redundancies or elsewhere.

I expect Macquarie's innovation in the green investment space will see it continue to outperform the market over the medium term, although I'd rate the stock a hold for now given its electric recent run.