This article was originally published on Fool.com. All figures quoted in US dollars unless otherwise stated.

This article was originally published on Fool.com. All figures quoted in US dollars unless otherwise stated.

Investors could be growing uncertain as the Nvidia trade appears to have unwound. Despite the company's recent near-perfect earnings report, investors are selling the stock as doubts rise about its high valuation.

So investors could be wondering where to invest next. These three Motley Fool contributors have suggestions on three stocks that have a higher likelihood of moving up: Meta Platforms (NASDAQ: META), Monday.com (NASDAQ: MNDY), and Nu Holdings (NYSE: NU).

Investors shouldn't ignore this cash cow

Jake Lerch (Meta Platforms): With Nvidia losing some steam in recent weeks, I'm turning my attention away from the king of artificial intelligence (AI) and toward the king of digital advertising, Meta Platforms.

Its stock has flown under the radar for much of 2024. While Nvidia and other high-profile AI stocks have grabbed headlines, Meta has skyrocketed 45% year to date. That makes it the fifth-best performing stock in the Nasdaq 100.

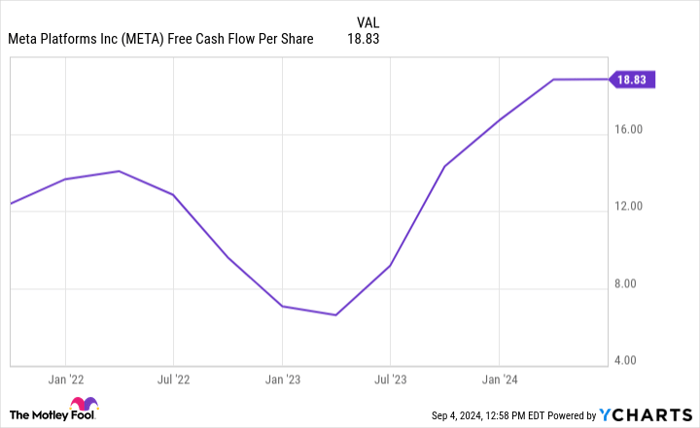

What's more, its surge is thanks to good, old-fashioned execution. Meta, with its more than 3 billion daily average users across its Facebook and Instagram platforms, continues to stack cash like an ice cream shop stacks scoopfuls during a heat wave.

The company generated nearly $50 billion in free cash flow over the last 12 months -- almost $19 a share.

META free cash flow per share; data by YCharts.

With so much cash pouring in, the company's balance sheet is rock-solid: over $58 billion in cash and equivalents with only $38 billion in debt, for a net cash position of about $20 billion. With so much free cash flow, Meta has now started returning a sizable portion of that hoard to investors.

In February, Meta announced its first-ever dividend, a regular quarterly payment of $0.50 a share. At the current price, that's a dividend yield of only 0.4%. Yet it shouldn't be ignored. Moreover, management also expanded its share buyback program to $50 billion.

In combination, these two measures, along with Meta's ample free cash flow, are why investors should consider the stock as a suitable alternative to Nvidia. Simply put, this cash cow is too big to ignore.

This stock is poised for years of profitable growth

Justin Pope (Monday.com): Every software stock looked like a winner in 2021, but higher interest rates have created a more challenging economy in which investors have seen the cream rise to the top.

Monday.com has proved itself to be a winner, which should have investors salivating at the company's still-bright long-term prospects. It's a software-as-a-service (SaaS) business that sells diverse and easily customizable work-management software.

When Monday.com went public, it wasn't clear that companies would truly stick to its product, but the results speak for themselves. Its excellent revenue growth includes a 34% year-over-year increase in the second quarter.

Monday.com has a 114% net revenue retention rate among customers that spend over $50,000 on the platform, and the number of companies spending that much grew faster than revenue did in the second quarter, up 43% year over year. There are now roughly 225,000 companies using Monday.com, a large pipeline that will begin to generate significant revenue.

The financials are improving as the business grows, too, with $261 million in free cash flow over the past four quarters on $845 million in sales. The company has $1.3 billion in cash and no debt, and it is profitable under generally accepted accounting principles (GAAP) over the past few quarters.

So Monday.com is no longer a speculative stock; it's a financially stable company that could enjoy strong earnings growth.

It's among some of the more expensive technology stocks on Wall Street, but quality is rarely cheap. Shares trade at an enterprise-value-to-sales ratio of just over 11, still far less than Palantir and CrowdStrike. Long-term investors can still buy Monday.com today and enjoy years of strong investment returns from profitable growth.

Consider following Warren Buffett's team into this Latin American fintech

Will Healy (Nu Holdings): When looking for new bull markets, undervalued stocks can be an excellent place to start. Among fintechs, perhaps few are less understood by U.S. investors than NuBank parent Nu Holdings.

The stock attracted early attention from Warren Buffett's Berkshire Hathaway, which bought it after its initial public offering. But despite attracting Buffett's interest, most U.S. investors can be forgiven for not knowing Nu.

Even though it is the largest digital bank outside of Asia, most of its customers are in Brazil. Now, with its success there, it seeks to repeat its formula in Mexico and Colombia.

Unlike in the U.S., Latin American banking was traditionally dominated by a small number of banks. The sway these banks held over their countries left large percentages of the population with neither bank accounts nor credit cards.

NuBank has changed this by issuing credit cards to millions of previously unbanked customers. Also, as a digital bank, the lower overhead costs that come with not operating branches have helped it build a competitive advantage. So successful is its approach that nearly 21 million of its 105 million customers opened their first Nu account over the last year.

Not surprisingly, such growth has appeared in its financials. In the first two quarters of 2024, revenue of $5.6 billion grew 60% compared with the same period in 2023.

During that time, Nu kept operating expenses in check. That allowed it to earn $866 million in net income in the first half of 2024, 136% more than in the first six months of 2023.

Investors have begun to take notice. The stock rose steadily over the last year, more than doubling over the last 12 months. Still, despite that increase, it sells at a price-to-earnings ratio (P/E) of 45, a low level considering the triple-digit profit growth for the year.

All in all, such conditions indicate undervaluation, implying its rally can continue. If investors can overlook the different financial culture in Latin America, they can still profit from this tremendous opportunity.

This article was originally published on Fool.com. All figures quoted in US dollars unless otherwise stated.

This article was originally published on Fool.com. All figures quoted in US dollars unless otherwise stated.