The APM Human Services International Ltd (ASX: APM) share price is an opportunity I'm excited about because of how cheap it has become. The S&P/ASX 300 Index (ASX: XKO) share hit a 52-week low this week. In this article, I'm going to tell you why I made a (relatively small) investment.

APM isn't a well-known business on the ASX, though it has a market capitalisation of over $1 billion.

It operates in 11 countries, including Australia, the UK, Canada, the US and Germany. Each year, it supports more than 2 million people of all ages through its service offerings which include assessments, allied health and psychological intervention, medical, psycho-social and vocational rehabilitation, vocational training and employment assistance, and community-based support services.

There are three reasons why I think this ASX 300 share looks good value right now.

Image source: Getty Images

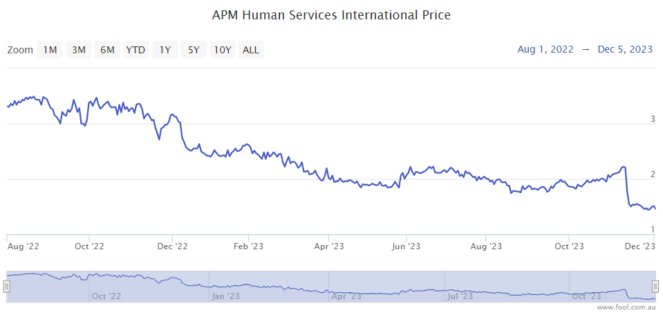

The APM share price is significantly down

I'm interested in investing in growing businesses. I'm particularly interested in those companies when the share price falls heavily.

The APM share price is down 60% since August 2022 and it's down 35% since 9 November 2023.

The company said it's expecting first-half earnings in FY24 to be lower than the first half of FY23 because of "continued record low levels of unemployment in Australia and the UK, resulting in lower client flows into employment programs, together with higher comparable interest costs and taxes."

However, it is expecting a stronger FY24 second-half earnings performance compared to the first half, based on "operational efficiencies implemented during the first half, continued growth of the health businesses, timing of new contracts and the historic second half skew."

According to the estimate on Commsec, the APM share price is valued at just 8 times FY24's estimated earnings and under 7 times FY25's estimated earnings.

Good revenue prospects

The employment market can't really get much stronger than it is, whereas there's a fair chance that unemployment could tick upwards amid the current conditions which could be a boost for the ASX 300 share's revenue and earnings.

APM also noted the UK has extended and expanded its 'restart scheme' in England and Wales for two years to June 2026. APM delivers two "prime restart" contracts in Greater Manchester and Central and West London and a further sub-contract in West Central.

The company has noted there are no major contracts due for renewal in FY24 or FY25, which suggests to me that its existing revenue is fairly supported.

I think there's also potential for it to expand in its existing markets and potentially expand into new markets.

Strong dividend income from the ASX 300 share

I like the cheap valuation, and this has a bonus effect of significantly increasing the dividend yield.

The estimate on Commsec shows a possible dividend yield of 9.2 cents per share, which would translate into a grossed-up dividend yield of 9.4%. That's with a dividend payout ratio of just 51%, so that would leave plenty of profit and cash flow within the business to improve itself.

Hopefully, the APM share price can rise from here, but I can receive large dividends until then.