The BHP Group Ltd (ASX: BHP) share price has proven resilient in the past, bolstered by a large and diverse portfolio of assets. Yet, the company's shares are still in the dirt compared to a year ago.

At their last closing price, shares in BHP commanded a $47.27 price tag — roughly 10% lower than their going price a year prior. It appears investors are cooling their jets on the mining giant as commodity prices are dialled down to a gentle simmer.

Is it a chance to add this formidable Australian miner to the shareholding cabinet? Or is it better to leave it in the dust? We asked two of our Foolish writers to provide the bull and bear argument for one of the largest companies on the ASX — enjoy!

What's to like about BHP shares now?

By Monica O'Shea: I am positive about the BHP share price in the long term.

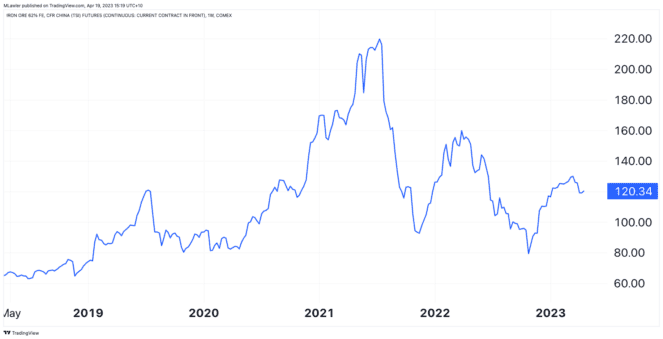

The iron ore price is a major factor that weighs on BHP shares on a regular basis. While the commodity has been volatile recently amid China's plan to cap domestic output on steel, it is still far higher than its one-year low of $81.50 in November.

At the time of writing, iron ore is fetching US$121 a tonne. Late last week, ANZ commodity strategists Daniel Hynes and Soni Kumari said China's commodity imports for March were surprisingly strong, commenting "Steel production is recovering, which could keep iron ore imports relatively steady."

On another note, I believe BHP's takeover of OZ Minerals Ltd (ASX: OZL) will broaden the company's earnings base from copper. The conductive commodity accounted for US$2.8 billion of BHP's underlying EBITDA in the first half of FY23, while iron ore contributed US$7.6 billion.

BHP has also recently received positive coverage from brokers. Macquarie has placed an "outperform" rating on BHP shares with a $52 price target. Meanwhile, Goldman Sachs has a hold rating on BHP with a $50.40 price target.

Another recent good sign for BHP is insider buying. BHP director Gary Goldberg has recently lifted his stake in the company, which could indicate he is seeing positive signs for the BHP share price going forward.

Finally, I believe BHP could be worth holding for its dividend. Despite the BHP dividend falling in March 2023, overall, the company pays a very reasonable dividend yield when you look across ASX 200 shares.

Goldman is tipping BHP to pay a final dividend of US$1.21 a share in FY23, up from 90 cents in the first half of the financial year. This equates to $3.14 Australian dollars and represents a dividend yield of 6.6% based on the current share price.

Motley Fool contributor Monica O'Shea does not own shares in BHP Group Ltd.

What's not to dig about this mining giant?

By Tristan Harrison: I think the best time to buy an ASX mining share like BHP is when the share price is at a cyclical low when the commodity price has fallen.

No one can know what commodity prices are going to do next month or even next year, but I don't think BHP is at a low point.

When we look at the BHP share price over the past six months, it has risen by around 16%. Since the middle of March, BHP shares have been flat. Yet, the iron ore price has dropped several dollars per tonne to around US$120 per tonne.

Iron ore has been the key earnings generator for BHP over the last few years, but China's demand may not be enough to push the iron ore price any higher from here. In fact, it wouldn't surprise me if the iron ore price fell by another US$10 per tonne over this year.

There's also the new China Minerals Resources Group (CMRG) which is looking to do much of the Chinese purchasing of iron ore. This means CMRG could have a lot of buying power and will try to negotiate a lower iron ore price with the ASX mining shares, like BHP. Time will tell how much of an effect this has on the iron ore price.

BHP shares could continue to pay decent dividends over the longer term, but Commsec numbers suggest that the company's dividend is going to be cut in FY23 to $3 per share.

With the company having a market capitalisation of $228 billion according to the ASX, I think it will be tricky for the business to grow strongly because of its enormous size.

Motley Fool contributor Tristan Harrison does not own shares in BHP Group Ltd.