This article was originally published on Fool.com. All figures quoted in US dollars unless otherwise stated.

After starting 2025 poorly, shares of Nvidia (NASDAQ: NVDA) have rallied impressively in the past three months. The chipmaker hit a 52-week low on April 7, and it has since shot up a remarkable 69% since then to become the first company in the world to achieve a $4 trillion market capitalization.

Nvidia's recent jump isn't surprising, as the stock's dip earlier in the year didn't seem justified considering the outstanding growth it has been consistently clocking on account of the terrific demand for its artificial intelligence (AI) chips.

Nvidia is trading at a rich valuation once again

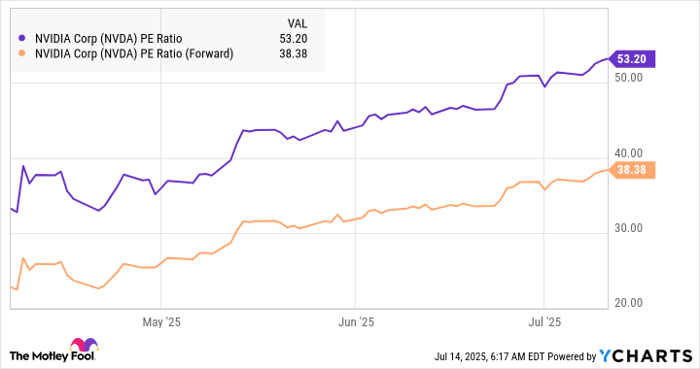

Nvidia stock's surge in the past three-odd months has made it expensive. This is evident from the following chart.

NVDA PE Ratio data by YCharts

Investors were getting a great deal on this fast-growing company in early April when its trailing price-to-earnings (P/E) ratio was in the low 30s, well below its five-year average earnings multiple of 70. The forward P/E ratio of less than 25 was even more attractive. The chip giant was trading at a nice discount to the tech-laden Nasdaq-100's average earnings multiple of 32 at that time, and savvy investors who bought the stock then are sitting on impressive gains as of this writing.

The good part is that Nvidia still has the ability to justify its expensive multiples and deliver more gains to investors in the future thanks to the multiple catalysts it is sitting on. From AI chips to accelerated computing to cloud gaming to enterprise software, Nvidia is set to benefit from several multibillion-dollar end markets that could help it keep growing at a solid pace for a long time to come.

Investors would do well to look at the bigger picture

Consensus estimates are projecting a 53% increase in Nvidia's revenue in fiscal 2026 to almost $200 billion. The company's data center business, which produced 88% of its revenue in the previous quarter, is going to account for a huge chunk of its top line in the ongoing fiscal year. Assuming Nvidia's data center business produces 90% of its top line in fiscal 2026, its revenue from this segment would land at $180 billion.

That would be a 56% increase over the previous fiscal year. This robust growth is being driven by the huge demand for Nvidia's AI graphics processing units (GPUs) which are being deployed in data centers for AI model training and inference purposes. Nvidia is expected to remain the biggest player in the AI chip market with an estimated market share of 80% to 85%, according to Bank of America.

Bank of America analyst Vivek Arya points out that the scale of Nvidia's customer base and its control over the supply chain will ensure that the chipmaker remains the top dog in this lucrative market. That's precisely the reason why Nvidia's data center business still has a lot of room for growth. According toMcKinsey, a whopping $5.2 trillion is expected to be spent on AI data centers by 2030, along with an additional $1.5 trillion on data centers for handling non-AI workloads.

The consulting firm also points out that the largest chunk of this projected investment -- 60% -- will go toward companies that design and manufacture chips and computing hardware. That could put Nvidia's potential data center chip revenue opportunity at a whopping $4 trillion after five years, much more than the revenue that the company is likely to generate in the current fiscal year.

Even if Nvidia loses ground in the data center chip market to its rivals, it can still witness exponential growth in this segment over the next five years that could send its revenue soaring. At the same time, demand for the company's enterprise AI software solutions, which help customers build AI agents and other applications, apart from helping them manage their AI infrastructure to ensure productivity and security, has been growing at a nice clip.

In February 2025, Nvidia management pointed out that its enterprise revenue almost doubled year over year on a quarterly basis as customers are deploying its solutions to fine-tune their AI models and to develop agentic AI applications, among others. The company claims that its generative AI software platform is helping customers to significantly increase accuracy and reduce the response time of their large language models (LLMs).

With the enterprise AI market expected to generate $104 billion in revenue in 2030, it won't be surprising to see this business move the needle in a significant way for the company in the long run.

Investors would do well to look past analysts' estimates and the valuation metrics, as Nvidia seems to be at the beginning of a remarkable growth curve even after the scintillating gains that it has recorded in revenue and earnings in recent years. Nvidia's potential revenue opportunity is massive enough to help it crush the market's expectations, and that could fuel this AI stock's rise to even a $10 trillion valuation in the next five years.

This article was originally published on Fool.com. All figures quoted in US dollars unless otherwise stated.