The Federal Government has warned Australians in retirement about a campaign of Centrelink age pension misinformation.

Services Australia has issued a statement about fake information circulating online purporting to announce changes to pension requirements.

The agency said:

There are unofficial websites and social media accounts spreading Centrelink misinformation online.

These websites are called clickbait.

Clickbait websites and social media accounts might say there are new document requirements for Centrelink pensioners; there are new eligibility and verification processes for Age Pensioners; your Centrelink payments will be cancelled, suspended or halted if you don't meet new requirements or guidelines; you'll get a fine or a debt if you don't take action.

These aren't true.

Services Australia said other Centrelink age pension misinformation includes new 'bonus' payments to help with the cost of living.

The agency said:

They offer varying amounts of money, including $750, $1,800 and $4,100. These payments don't exist.

People are sharing these websites on social media, thinking the information is real.

If the website URL doesn't end in .gov.au then it isn't an official government website. It could be a scam.

The only genuine Services Australia and myGov websites are servicesaustralia.gov.au and my.gov.au.

Image source: Getty Images

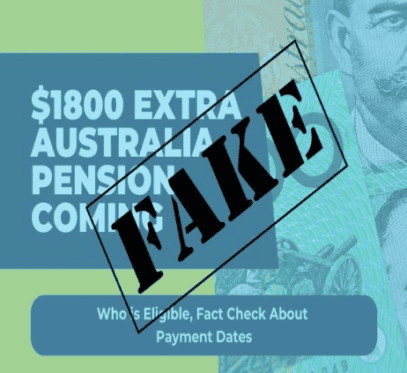

What does the fake information look like?

Services Australia has provided an example of how some of the Centrelink age pension misinformation is being presented.

Services Australia recommended that pensioners and retirees go to its website for genuine Centrelink payment information.

How much is the age pension?

The Australian age pension is currently $29,874 per year for singles and $45,037.20 per year combined for couples living together.

That includes the maximum basic rate, the maximum supplement, and the energy supplement.

Australians are entitled to receive the age pension when they reach 'retirement age', subject to asset and income tests.

The retirement age is 67 years for people born on or after 1 January 1957.

There are other eligibility criteria, including residency rules.

If you earn or own too much for the full pension, a sliding scale will determine a part payment up to certain limits.

When will the next change to the age pension occur?

The age pension is indexed to inflation and changes twice per year.

As we reported, the last indexation increase occurred on 20 March.

That's when the full payment for singles, including all supplements, rose to $1,149 per fortnight.

The full payment for couples living together rose to $866.10 per partner per fortnight.

The age pension is due for its next indexation rise on 20 September.

What about the assets and income tests?

The upper thresholds for the asset and income tests change twice per year on 20 March and 20 September.

They are also indexed to inflation.

The lower thresholds change once per year on 1 July.

The new lower limits have not yet been announced by the Social Services Department.

This is the only change relating to age pension requirements that is coming up in the near future.

What are the current rules?

In terms of the assets test, single homeowners are eligible for the full pension if their assets (excluding their home) are worth less than $314,000. Non-homeowner singles are eligible if their assets are worth less than $566,000.

Single homeowners are eligible for a part-payment if their assets are worth more than $314,000 but less than $697,000. Non-homeowner singles are eligible if their assets are worth more than $566,000 but less than $949,000.

Couple homeowners living together are eligible for the full pension if their assets (excluding their home) are worth less than $470,000. Non-homeowner couples are eligible if their assets are worth less than $722,000.

Couple homeowners living together are eligible for a part pension if their assets are worth more than $470,000 but less than $1,047,500. Non-homeowner couples are eligible if their assets are worth more than $722,000 but less than $1,299,500.

The assets test incorporates ASX shares, international stocks, bonds, investment properties, superannuation, and cash savings.

In terms of the income test, single pensioners are allowed to earn a maximum of $212 per fortnight and still receive the full payment.

Singles may be eligible for a part-payment if they earn more than $212 but less than $2,510 per fortnight.

Couples living together can earn a maximum of $372 combined per fortnight and still qualify for the full payment.

Couples living together may be eligible for a part-payment if they earn more than $372 but less than $3,836.40 combined per fortnight.