The oOh!Media Ltd (ASX: OML) ("OML") share price fell 1% to $4.75 following the publication of its half-year results this morning. Revenues rose 11% to $192 million, and statutory net profit after tax rose 1.6% to $9.3 million. OML reported that a change in business model, due to investment in digital technology, resulted in a substantially higher depreciation charge, which kept profits low despite rapidly growing revenues.

OML reported 6 cents per share in earnings and declared 3.5 cents per share in fully franked dividends. The company ended the half year with $9.5 million in cash and approximately $134.5 million in debt, for a net debt position of $125 million.

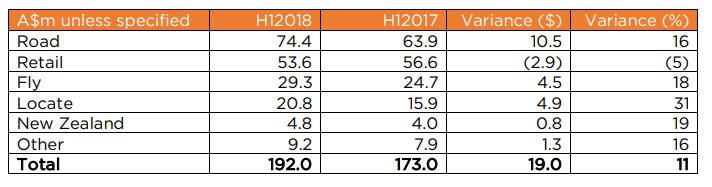

Management reported strong revenue growth in each of the company's advertising niches in the first half of the year. Most segments grew at double digits, albeit with Retail advertising struggling due to reduced spending across the category from some major retailers.

The strong performance, however, was not matched by growth in profits, with management stating that higher staff and depreciation costs kept profits restrained. The business is expected to benefit from operating leverage in the future, as growing revenues from investment in the current and previous years, lead to wider profit margins.

oOh!Media also announced progress with its Adshel acquisition, with that purchase expected to complete in the latter half of calendar year 2018. Adshel will add 21,000 poster faces and 800+ digital screens (among other assets) across a business that reaches 87% of New Zealanders and 92% of Australians. The acquisition looks a good one but is still dependent on regulatory approval.

For the business' outlook for the rest of the year, management stated that Out of Home revenues were expected to remain strong for the rest of the year. Management was forecasting underlying earnings before interest, tax, depreciation and amortisation (EBITDA) of $94 million to $99 million for the full year, a significant increase compared to $37.9 million in this half. This guidance excludes the costs and benefits related to the proposed acquisition of Adshel but does include between $30 million to $40 million of capital expenditure.

At today's prices, oOh!Media is valued at over a billion dollars or somewhere around 40x estimated full-year profits. It is a good and growing business, but the bull case for getting value out of OML shares appears to be that recent investments continue to deliver revenue growth, and the company is able to widen its margins and grow profit substantially in the coming years. It will likely take several years for the company to deliver the full value from these investments and acquisitions, and as a result, I believe oOh!Media is only suitable for investors with ~5-year time frame.