The G8 Education Ltd (ASX: GEM) share price fell 15% to $2.06 this morning after the company released its interim results. The cause of the price fall was a weak half year result combined with a sharply lower dividend and a mediocre outlook. Here's what you need to know:

- Revenue rose 7% to $393 million

- Net profit after tax fell 22% to $24 million

- Underlying net profit after tax fell 24% to $25.6 million

- Underlying earnings per share down 32% to 5.68 cents per share

- Dividends per share of 4.5 cents

- Outlook for business conditions to not improve until late in 2019

- May be an improvement to second half performance if occupancy keeps improving &

due to impact of new Child Care Subsidy

So what?

I wrote earlier this year in March that I thought G8's dividend was clearly unsustainable. That has proven the case, with the company cutting its dividend substantially to today's level of 4.5 cents per share.

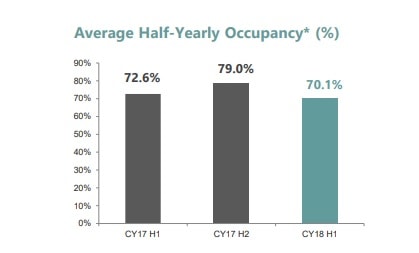

A childcare business is all well and good when occupancy is improving, and prices are rising, because this leads to wider profit margins and booming profits. The company can then borrow substantially more to invest in new centres, creating a virtuous cycle of growth. However, G8 is several years past that point. Now, additional competition has sprung into being and pricing and occupancy are being pressured, with staff costs are rising. This has lead to lower occupancy and sharply lower profits:

G8 has an annual cycle to its business governed by the school holidays, with the second half always being a bigger contributor to earnings (due to the higher occupancy in the above chart). As a result I think it is likely that the current result could be an overreaction by the market, which often sells off G8 on its first half results.

Now what?

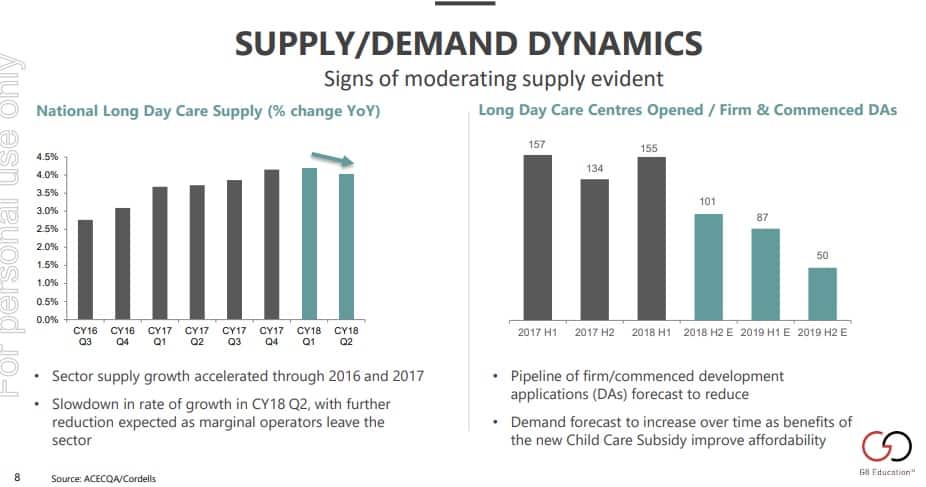

However, there's no question that the outlook for childcare businesses remains challenging, with this chart in particular showing that supply may be just starting to peak:

Having said that I do note that it's not until results head south that G8 has started to talk seriously about supply and demand in the industry. There's also a bit of a bad taste in issuing 438,000 performance rights to executives after a couple of years of what I think is pretty mixed performance.

I expect that G8 may continue to reduce debt over the next year or two. Generally speaking it can take several years for excess capacity to work its way out of an industry, so the most prudent thing would be for G8 to build up a financial reserve to weather what could potentially be several years of mediocre business conditions.

Overall, I find G8 interesting at current prices, but with oversupply still working its way through the system, I don't see any compelling reason to race out and buy G8 today. Using dividends alone as a rough rule of thumb, I'd be inclined to demand a 5% sustainable yield or more from a mature company of this type, so G8 shares may have a way to fall yet before they become a bargain.