The ability to understand financial statements is a significant benefit to investors. They can use this knowledge to analyse the performance of companies they are considering investing in, providing a sound basis for investment decisions.

Image source: Getty Images

What is a balance sheet?

A balance sheet or a 'statement of financial position' details a company's assets, liabilities, and shareholder equity at a given time. It provides a snapshot of what a company owns and owes and the amount shareholders invest.

Assets

The first column on a balance sheet shows a company's assets. These are things of monetary value that a company owns that can be measured objectively. Examples include cash in the bank, short-term investments, stocks, trade debt, property, and even petty cash.

There are also asset classes such as current assets (those expected to be converted to cash within a year), fixed assets, and intangible assets.

Liabilities

In the other column, you'll find liabilities. These are debts or payments that a company expects to pay out in the future. A company owes liabilities to others, such as employees, suppliers, creditors, tax authorities, etc.

The company must pay its liabilities under certain conditions and within specific timeframes. Current liabilities, for instance, are those due for payment within a year. Examples include overdrafts, short-term loans, and creditors.

There are also long-term liabilities such as long-term loans, secured bills, directors' loans, the residual value on leases, and more.

Shareholder equity

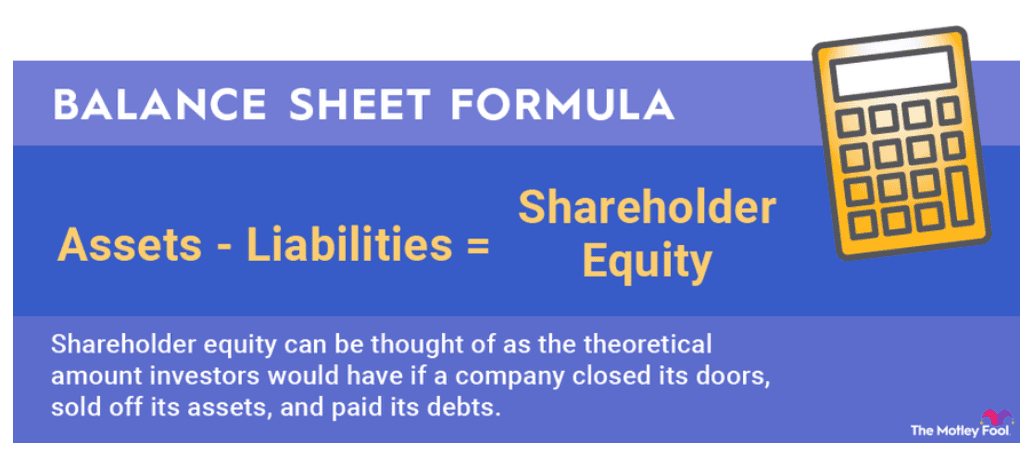

Another essential piece of information is shareholder equity. This is the remaining value of assets available to shareholders when the liabilities have been paid off. Assets minus liabilities equals shareholder equity.

In other words, a company's equity represents retained earnings and funds contributed by its shareholders.

When you know a company's shareholder equity, you can determine answers to various vital questions, such as: How much cash is available after the company has paid all its liabilities? How long can it last if its debts become due?

We can further divide assets into current assets, which are convertible to cash within a year. Non-current assets are more permanent. Similarly, liabilities can be divided into current liabilities (due within a year) and non-current liabilities, obligations due in more than one year.

The heading can also be an important part of the balance sheet. It sometimes has an alternative name, such as 'statement of financial position' or 'statement of condition'.

On the balance sheet, assets – liabilities = equity.

Image source: The Motley Fool

As sales grow, a more extensive asset base (perhaps allowing for high inventory levels and more fixed assets) will be required. As assets grow, liabilities and equity tend to grow, so the company's financial position stays balanced.

What are the 3 types of balance sheets?

- Comparative balance sheets: These include a side-by-side comparison of the entire balance sheet report of a current and previous accounting period. This can help identify trends over time.

- Vertical balance sheets: These are presented as a single column of numbers, beginning with assets, liabilities, and shareholders' equity. This is more common when fewer line items are presented.

- Horizontal balance sheets: These use extra columns to present more detail about the business's assets, liabilities, and equity. The horizontal balance sheet is most useful when several line items are presented since the format allows for additional line items.

Why are balance sheets important to investors?

The balance sheet provides an overview of a company's financial position and what it owns and owes. It gives a view of the company's assets and liabilities and answers questions about whether it has a positive net worth, enough cash to cover its obligations, and how highly indebted it is.

Many important financial ratios used in fundamental analysis are also drawn from the balance sheet, such as liquidity, solvency, and profitability ratios. These ratios can give investors a general outlook for the company.

It can be helpful for investors to compare balance sheets across time periods as this can tell a story about the business conditions the company is facing. Investors want to ensure companies can pay off short-term debts, i.e. that current assets exceed current liabilities. They are also looking for shareholder equity to increase over time.

What is a profit and loss (P&L) statement?

The profit and loss (P&L) statement is a crucial piece of the puzzle when discerning a company's financial strength. The P&L statement is separate from the balance sheet.

The P&L statement (also known as an 'income statement' or 'statement of financial performance') summarises all the revenues, costs, and expenses a company has incurred during a specific time period. Typically, a P&L statement is calculated per quarter as well as annually.

P&L statements provide information about a company's ability or inability to generate profit by increasing revenue, reducing costs, or both. Comparing P&L statements from different accounting periods is essential, as any changes over time can be more meaningful than the raw numbers.

Types of P&L statements

Companies can prepare P&L statements using the cash method or the accrual method.

Cash method: This relatively simple method only accounts for cash received or paid. Transactions are recorded as revenue whenever money is received and as liabilities when cash is used to pay bills or liabilities. Often, people who want to manage their personal finances use the cash method.

Accrual method: Records revenue as it is earned. A company using the accrual method will therefore account for the money it expects to receive in the future. For example, a company that delivers a product to a customer records the revenue on its P&L statement, even though it hasn't yet received payment. Liabilities are also accounted for even when the company hasn't actually paid the expenses.

Top and bottom line

Two standard terms you'll hear concerning P&L statements are 'top line' and 'bottom line'. Top line refers to a company's revenues or gross sales. When a company has top-line growth, sales and/or revenue are increasing. The bottom line is the company's net income.

The company's operating costs and expenses are everything between the top and bottom lines. A healthy top line is one thing, but the bottom line will demonstrate a company's profitability. We can also call the bottom line net earnings or net profits.

Balance sheet vs. P&L statement

The P&L statement shows results over a defined period (such as a quarter or a year). The balance sheet, on the other hand, provides a snapshot of the business's performance at a given date.

If you want to stay on top of a company's financial performance, using both the P&L statement and balance sheet is essential.

These statements provide a record of a company's financial condition at the point in time that they were prepared. The balance sheet, comprising assets, liabilities, and equity, allows for an evaluation of a company's capital structure.

The P&L statement shows the company's realised profits or losses for the relevant period. Over time, it may indicate an ability to increase profit by reducing costs or increasing sales.

Although the balance sheet and P&L statement contain some of the same information, it is essential to remember that the balance sheet reports at a point in time while the P&L statement covers a period of time.

The P&L statement provides the answer as to whether the company was profitable over that period of time. The balance sheet, on the other hand, is broader, revealing the full value of what the company owns and owes.

Frequently Asked Questions

-

A balance sheet primarily consists of assets, liabilities, and shareholder equity. Assets are valuable resources the company owns, such as cash and investments. Liabilities represent the debts and obligations the company owes to others, such as loans. Shareholder equity is the residual interest in the company's assets after deducting liabilities, essentially showing the amount shareholders invest.

-

The purpose of a balance sheet is to provide a snapshot of a company's financial position at a specific point in time. It outlines what the company owns (assets), what it owes (liabilities), and the amount invested by shareholders (equity). Investors and analysts use the balance sheet to assess the company's stability, liquidity, and overall financial health.

-

The balance sheet and the P&L statement are both essential financial documents but serve different purposes and provide other information. The balance sheet gives a snapshot of a company's financial position at a point in time, showing its assets, liabilities, and equity. The P&L statement, on the other hand, summarises revenues, costs, and expenses incurred during a specific period, showing how well a company can generate profit over time.