How much do you need for a comfortable retirement? What a vexing question…

Of course, these days, it is difficult to know how much we really need for retirement. Gone are the times where 'defined benefit' retirement pensions are the norm.

A defined benefit pension works by giving its beneficiaries a defined income every year, rather than a return from an invested lump sum – in a similar formula as the Aged Pension.

Obviously, most people would prefer a defined income stream because it takes worries over share market crashes, bubbles, asset allocation and 'how much do I need' out of the equation.

What does modern retirement look like?

Unfortunately, most people still working aren't lucky enough to be on the receiving end of one of these kinds of pensions – especially if you work outside the public service.

For most of us, its 'defined contribution' all the way. That's another way of describing the 9.5% superannuation guarantee that almost every Australian worker is entitled to.

But (as alluded to above), this system (whilst less expensive for governments and employers) comes with its own limitations. That's partly why there is currently a debate raging about the merits of the proposed plan to lift the super guarantee to 12% (which is already legislated).

In conventional financial planning, older and retired Australians are advised to place a significant proportion of their assets in 'low risk' investments like bonds and term deposits.

That has worked well in the past. But interest rates are now at record lows across the world – which means that these 'safe' assets are now almost impotent in being able to deliver enough income to make it worthwhile to invest in them in the first place.

The 10-year Australian government bond yield is today at 1.04% (at the time of writing anyway). A competitive term deposit rate isn't much better at around 1.5%.

It's pretty hard to fund a decent retirement with interest rates like that – especially if you consider the effects of inflation.

And it's this beautifully terrible conundrum that is helping to stoke fears about retirement today, in my view.

What about younger people?

But according to reporting in the Australian Financial Review (AFR), it's younger people who are worrying the most about the future.

That's right!

The AFR quotes a study undertaken by National Australia Bank Ltd. (ASX: NAB) that finds it's the 30-49 age bracket that has the highest levels of anxiety about funding their retirement – which has actually increased over the six months to December 2019.

Providing for the family's future and worries about medical bills and expenses were also concerns. But it's the fear of not having enough that's really permeating the younger demographics.

But the NAB survey also noted another (slightly surprising) trend.

Once people have actually retired, fears about the adequacy of their savings subside somewhat.

The AFR report quoted NAB's Dean Pearson, who stated:

"The challenge we find is that most people when asked 'how much do you need to retire?' they say, 'more than $1 million', but when they actually end up retiring, they only have about $600,000 and they say they can get by on $600,000. We think people could be overestimating how much they will need".

Mr Pearson makes an interesting point. A million-dollar retirement portfolio does sound like a lot of money (and it is). But when you consider that a couple only needs to contribute $500,000 each, this sum becomes a lot more palatable. And if a couple finds themselves with a balance of $600,000 – it's still enough for a comfortable standard of living, especially if the individual or couple in question owns their own home.

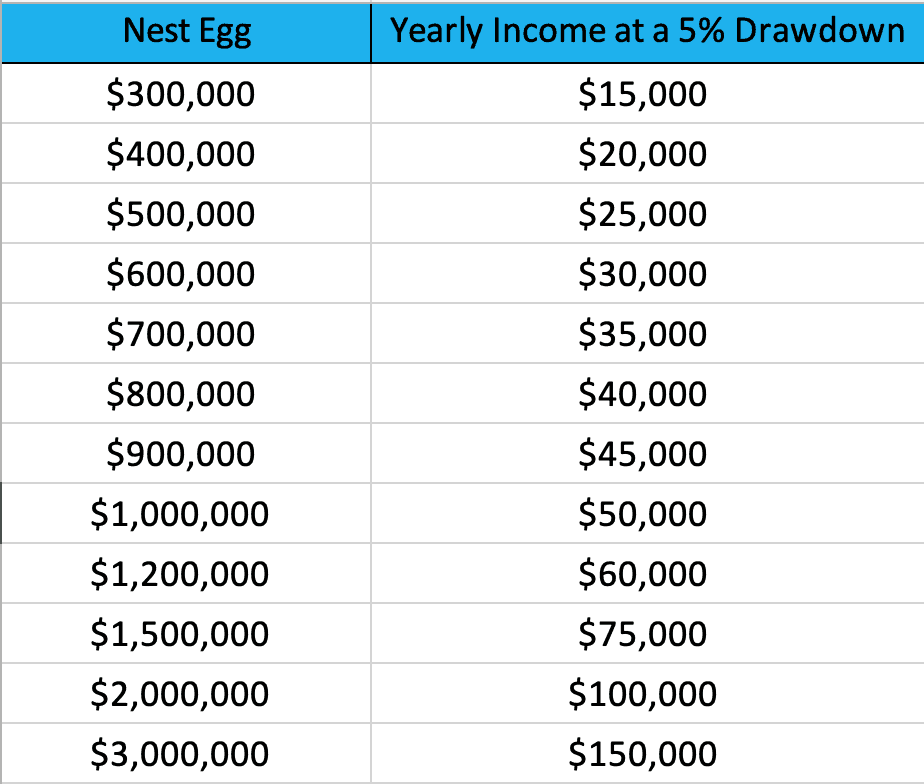

I've prepared this table that outlines how much you can expect to receive depending on how large your retirement savings are on a per annum basis.

Source: Yours Truly

It assumes a drawdown rate of 5% per annum which is roughly adequate to modestly preserve capital and absorb the effects of inflation over a long period of time (although this will vary on your individual circumstances and investment allocation, make sure to discuss this with a financial advisor!)

Bear in mind that the lower an individual or couple's super and asset balances are in retirement, the more likely they will be to qualify for a part or full Aged Pension – which can substantially supplement retirement income.

So why are young people more worried about affording an adequate retirement than those who are already retired?

The final observation of the NAB study perhaps explains this phenomenon. It outlines how loneliness afflicts those in younger age brackets at a far more pervasive rate that older Australians:

"Young people aged 18-29 indicated they were loneliest, scoring the issue 46.5 out of 100. Loneliness as an issue falls progressively in each age group, with the over 65s the least lonely scoring it 22.8 out of 100."

Being financially comfortable is only one ingredient in the recipe for a happy retirement. Looking at these numbers, I think the younger individuals surveyed are overestimating how much they might need in retirement because of feelings of loneliness.

If you're lonely in your younger years, you might picture an adequate retirement as one involving lots of holidays, trips, cruises and 'going out' – all of course very expensive pastimes. We might find those who instead spend their retirement in the company of family with friends who live around the corner are in fact far happier while also spending far less.

Foolish takeaway

Retirement is a complex question because of how many unknowns there are. None of us know exactly how long we're going to be blessed with life on this planet – and that intrinsically makes planning for our golden years difficult. It also inherently involves the acceptance of 'getting old' which most of us don't particularly enjoy contemplating either!

Finally, a comfortable and happy retirement involves far more than just money (although it remains an essential component, of course). So I think many younger Australians might be focusing too much on the financial side of things, and not on what really makes us happy as humans.

I think getting the balance right is the most important thing here. And as our older Australians tell us, once we're actually retired, things are usually not as bad as we might fear!