The AfterPay Touch Group Ltd (ASX: APT) share price is down 3% on the back of an operating update today that revealed more blockbuster growth in the U.S. market, progress in the early days UK market, and more strong performance in Australia.

For the 11 months to May 31 2019 it revealed underlying sales were up approximately 43% on the prior corresponding period to $4.7 billion with over 4.3 million active customers signed up.

In fact it signed up an incredible 7,900 customers per day on average over the period since December 31 2018. I don't think you'll find a credible business on the ASX growing anywhere nearly as quickly as this and I cannot remember seeing one having done so in the past.

Which begs the question as to why the share price is falling today? Maybe because there's just more sellers than buyers. But why are there more sellers than buyers?

Maybe because the market expected even stronger growth, or maybe it's a little disappointed about the lack of hard financial numbers out of the UK.

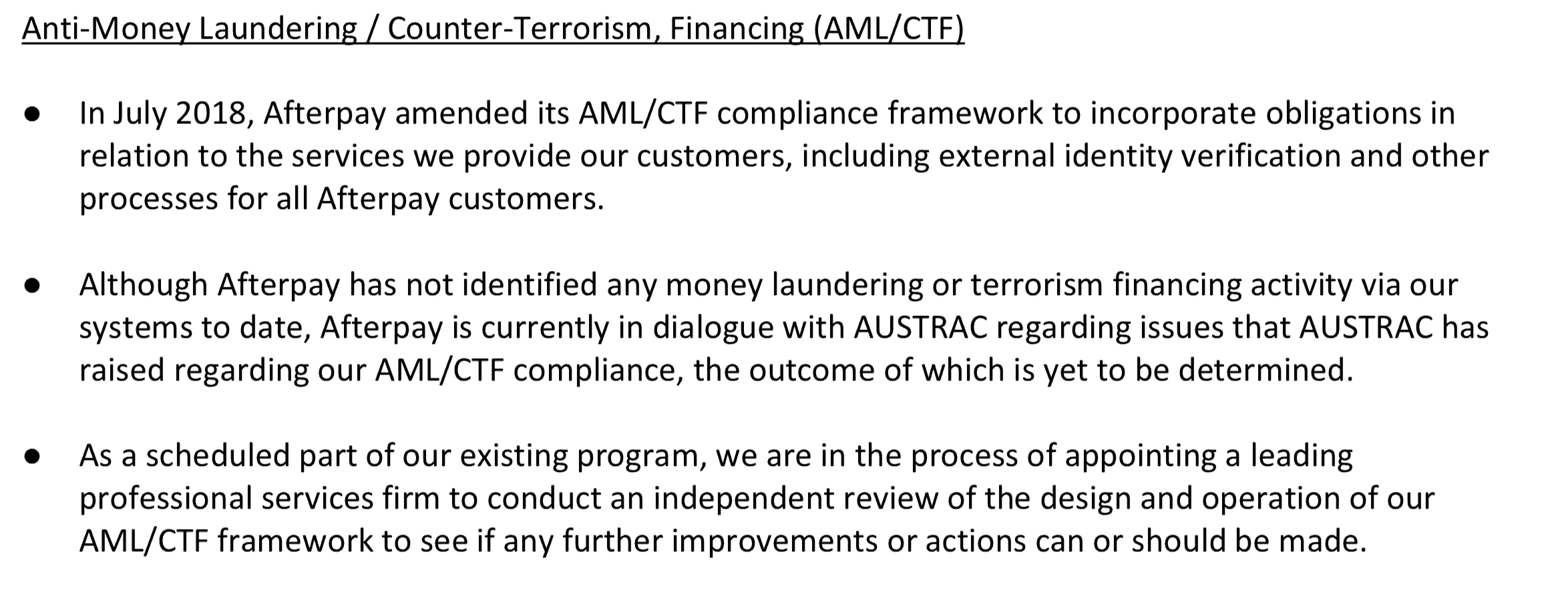

Another point for investors to consider today is that the company admitted the anti-money laundering regulator AUSTRAC has been paying close attention to Afterpay since July 2018 alongside its obligations under the onerous AML/CTF Act 2006.

In fairness this is something I've flagged as a potential risk in terms of increased costs before. Below is an extract from today's update.

Source: AfterPay investor presentation, June 6 2019

A couple of points to note on this, first, I am unclear as to whether AUSTRAC classifies AfterPay as a reporting entity under the terms of the AML/CTF Act 2006. However, given the update it looks more likely than not, and either way we know it considers Afterpay has obligations to AUSTRAC.

Another point to note is that it looks like AfterPay faces rising costs due its obligations as a reporting entity.

Firstly because reporting entities are obliged for example to report every suspicious transaction (i.e potential money laundering, proceeds of crime rick, etc) to AUSTRAC.

This I think includes every transaction greater than $10,000 and every transaction that a reasonable person would consider an AML risk for example.

So a reporting entity must demonstrate it has the systems and procedures in place to do this (i.e report a transaction over $10k). Quite a big task if you're doing as many daily transactions as AfterPay.

For example we recently saw AUSTRAC pretty much bring down the Commonwealth Bank of Australia (ASX: CBA) CEO from his job for its failure to report tens of thousands suspicious transactions in a timely manner to AUSTRAC.

Huge $700 million penalties also followed.

For clarity I am reading a bit between the lines on AfterPay's announcement, but we can see if it does come under the obligations of AUSTRAC it could face rising compliance costs in terms of its reporting processes. However, I don't expect the costs would be especially material.

It also admits it has appointed a 'leading professional services firm" to help it operate its AML/CTF framework with PWC in particular well known among the Big 4 consulting firms for this kind of work. And from professional experience I can tell you they don't come cheap, but again costs would not be that material and one off in nature.

Another point to note is that the AML/CTF Act 2006 has understandably onerous customer identity verification requirements.

After all if you're a criminal looking to launder money, you're most likely going to want to hide your ID.

For example I went to an over-the-counter FX exchange in Sydney recently to buy some Thai baht for a tropical holiday and the teller wanted to photocopy my ID, not for fun though, but because she's required to maintain an original copy under the terms of The Act.

Now it seems much of the verification procedures for lower risk transactions (i.e non OTC cash) can be automated (just imagine if AfterPay had to photocopy 4.3 million customers' ID) and AfterPay has agreed how it will verify ID with regulators via what seems a simple low-cost process, which is a major positive. For example, they're online tools such as Veda for this kind of thing and the announcement above also seems to reference the ID verification matter as being settled.

Outlook

Overall though it seems AfterPay could face some moderately rising costs under its AUSTRAC obligations and it's important for investors to note it faces huge penalties if it were to fail in meeting those obligations as we saw with the CBA recently. As you can imagine it's probably handed an almost blank cheque to the 'professional services firm' helping it sort out its policies and procedures to the regulator's liking.

Generally though please note this article is based on some reading between the lines and should not be used to make investment decisions. For full disclosure I do own a very small amount of AfterPay shares and the above will not lead me to sell or change my investment view.