The Getswift Ltd (ASX:GSW) share price has been annihilated, falling more than 60% to $1.16 (at the time of writing) upon its return to trade this morning. After almost a month in suspension, which we covered in chronological order here, here, here (quarterly report), and here, Getswift confirmed this morning that it was in compliance with the ASX listing rules.

Getswift was originally suspended because it had not informed the market of contracts that it lost last year that were reported in Fairfax media. Getswift could not – until today – confirm whether it was in compliance with listing rule 3.1 (Continuous Disclosure), and had to hire PriceWaterhouseCoopers (PWC) to conduct a review of the company's disclosure.

Contrary to what was insinuated in the Fairfax media article, Getswift does not appear to have lost any further contracts, and it stated as much to the market during its suspension. That said, the company stated that it is not always aware of whether a customer has quit its contract or is simply not using the Getswift solution.

However, Getswift also acknowledged that less than 50% of its contracts were currently earning revenue: "Almost 50% of GetSwift's Enterprise Client contracts have progressed through to early stages of the revenue generation phase."

Probably the thing that has surprised me most about Getswift is the similarities between it and fallen darling 1-Page Ltd (ASX: 1PG) – itself a titanic failure that recently became a medical marijuana stock. However, a closer look at both the 1-Page prospectus and the Getswift prospectus reveal that the same entities sponsored both listings. Cygnet Capital played a role in 1-page and a much larger role in Getswift.

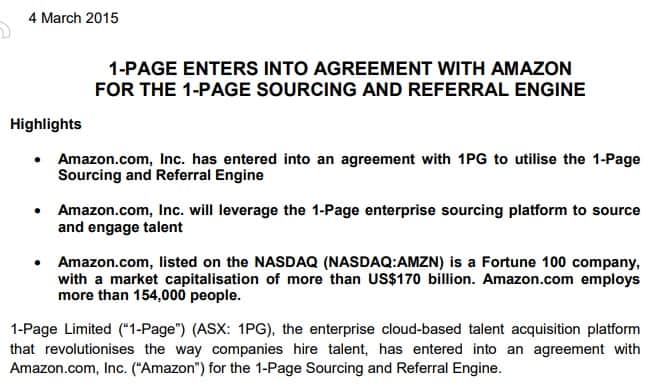

This makes comparisons between Getswift's announcements and 1-Page's announcements more concerning. 1-Page itself was famous for many large announcements with famous companies that did not end up showing any revenue. 1-Page struck a deal with Amazon, stating:

That's all the announcement said. There were no details provided of the terms of the arrangement or any forecast revenues. I recall the arrangement being criticised at the time, criticism that was subsequently borne out in business performance. However, the market was not nearly so sceptical as it should have been, and the same appears to be the case with Getswift.

Getswift also has a deal with Amazon, and surprisingly that deal has not attracted nearly as much criticism as some of Getswift's other deals like Fruit Box:

The announcements are virtually identical, and shockingly brief. Even more concerningly, the ASX subsequently called for further disclosure from Getswift over its Amazon deal, and Getswift stated:

"The extent of the services to be provided and the revenues to be derived will be generated from specific transactions agreed with Amazon pursuant to the Master Services Agreement. Due to the terms of the agreement the number of deliveries this agreement may generate is currently not determinable." (emphasis added).

In my opinion that is an outrageous announcement, given that Getswift shares virtually doubled on the first announcement. I am not surprised at all to see the share price totally unravel today following the AFR's criticisms and the company's lengthy suspension.

The more poignant question for shareholders now is whether the remaining deals – many of which appear similar to the above – are likely to generate any revenues. The Amazon deal in particular stands out because of Amazon's well-known and pugnacious attitude towards suppliers.

Jeff 'Your Margin Is My Opportunity' Bezos is famous for his unrelenting pressure on Amazon suppliers and employees in order to lift productivity and lower costs. I struggle to see how or why Amazon would rely on Getswift in any way rather than building its own software solution. Amazon is famous for having computer-optimized warehouses that maximise the walking efficiency of its product pickers, and I can't see why this obsessively performance-focused company would bring in an outsider – and an unproven startup like Getswift at that – to use its software.

A lack of disclosure also makes it hard to evaluate Getswift's contracts and business, especially since only 'almost 50%' of them are generating revenue. The overlap in financial backers involved in these companies also makes me pretty sceptical.

Motley Fool Hidden Gems advisor Claude Walker wrote last month that – if management stayed the same – he thought the fair value for Getswift shares was well below its cash backing per share, which is around 60 cents or so.

After the month that has just passed, I now agree with Claude completely. I think Getswift is a highly risky business that has built its name on hype and not business performance. Whether the company can subsequently go on to perform is an open question. However, I think Getswift is currently a very poor prospect and I would avoid it entirely.